No AI-discovered drug has ever received FDA approval. That sentence should sit uncomfortably next to every headline about Alphabet’s drug discovery spinoff.

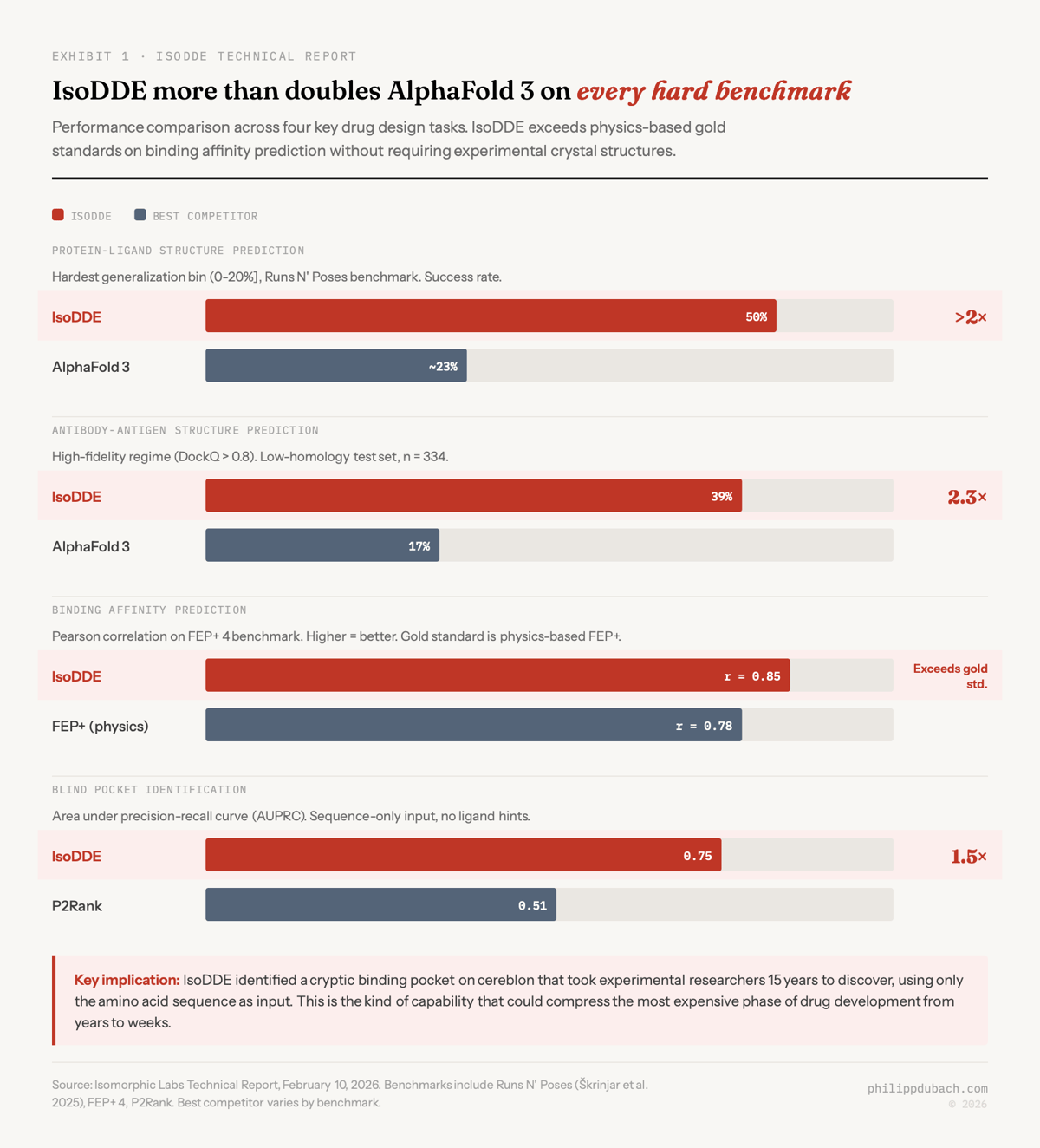

On February 10, Isomorphic Labs, the Google DeepMind spinoff focused on computational drug design, released IsoDDE: its Drug Design Engine. This isn’t a model or an AlphaFold upgrade. IsoDDE is a unified in silico drug discovery system that runs protein structure prediction, ligand binding, affinity estimation, and pocket identification in concert, generating in seconds what used to take days of physics-based simulation. On the hardest molecular prediction tasks, the “Runs N’ Poses” benchmark designed to test generalization to unfamiliar proteins, IsoDDE hits a 50% success rate. AlphaFold 3 manages roughly 23%. On antibody-antigen modeling, IsoDDE beats AlphaFold 3 by 2.3× and the open-source Boltz-2 by 19.8×. On binding affinity prediction, it achieves a Pearson correlation of 0.85, beating the physics-based gold standard FEP+ at 0.78.

I would assume that these are large enough improvements that the computational bottleneck in drug design may no longer be the binding question.

I would assume that these are large enough improvements that the computational bottleneck in drug design may no longer be the binding question.

What pharma believes

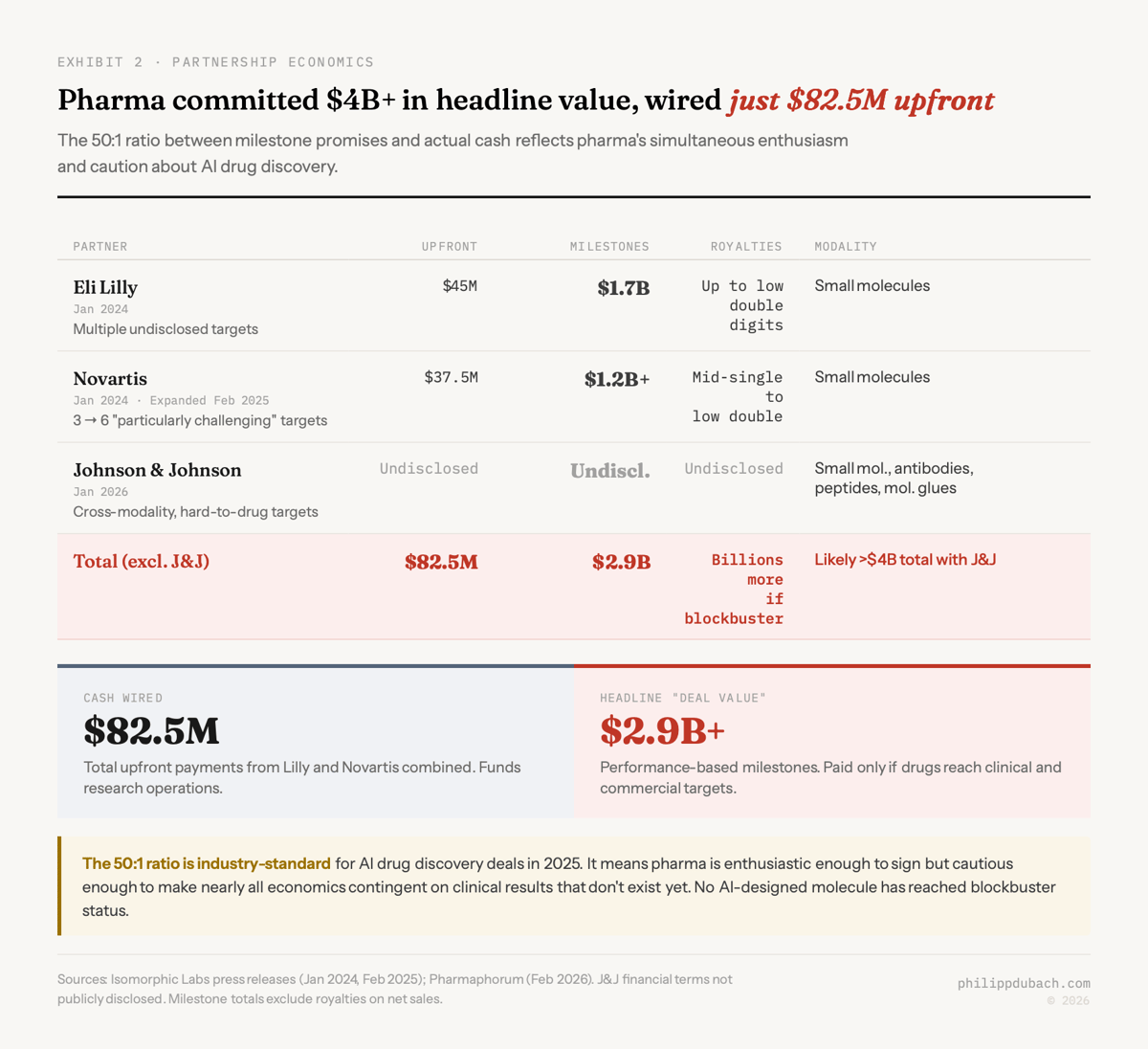

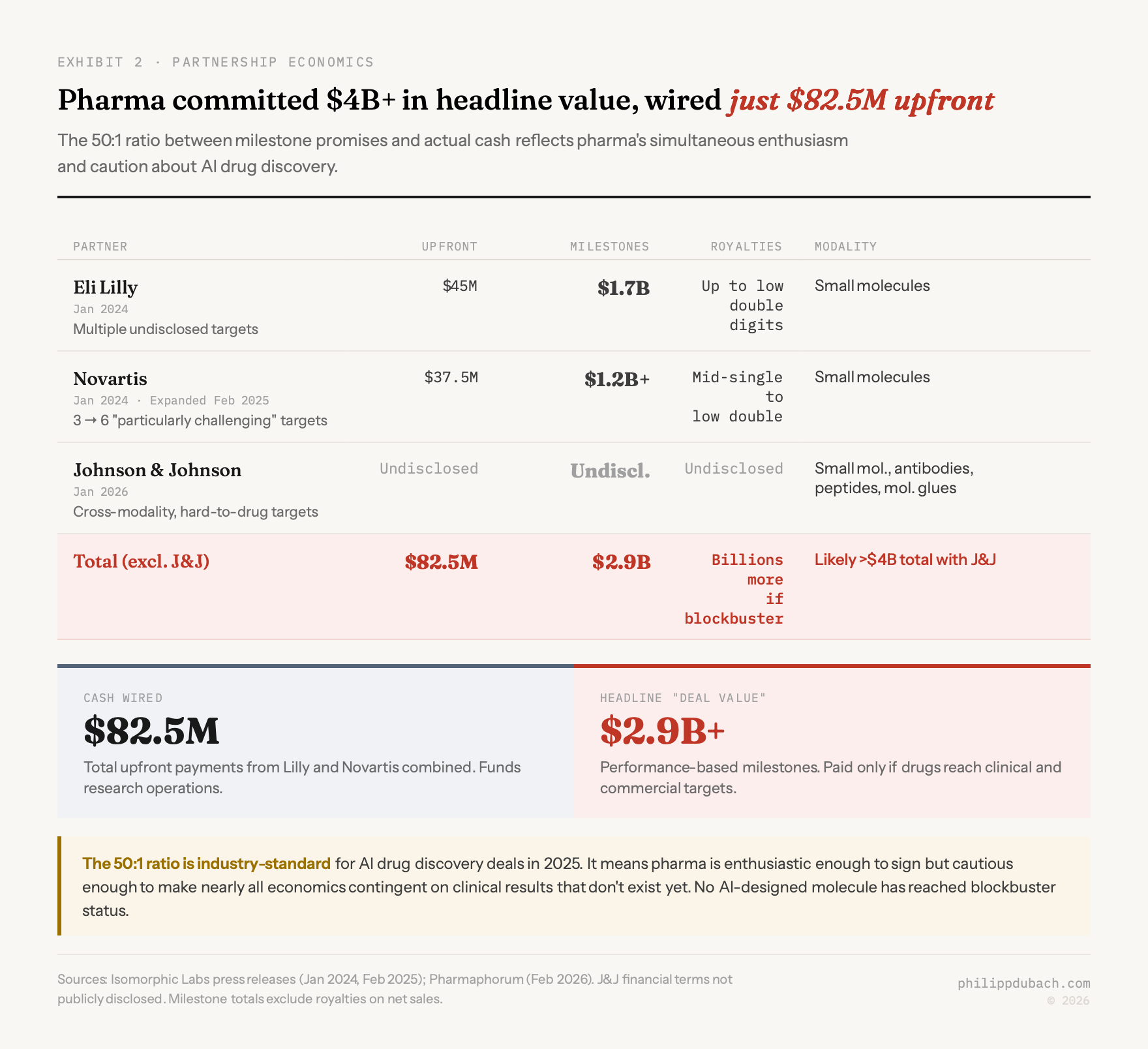

Isomorphic has signed partnerships with Eli Lilly, Novartis, and Johnson & Johnson worth a combined $4 billion+ in potential value. But look at the structure. Lilly paid $45 million upfront against $1.7 billion in milestones. Novartis paid $37.5 million upfront against $1.2 billion. That’s a 50:1 ratio between what pharma promises in biobucks and what it actually wires.

This ratio is standard across AI drug discovery deals in 2025. Pharma is enthusiastic enough to sign but cautious enough to make nearly all the economics contingent on clinical results that don’t exist yet. The upfront payments fund research. The milestone payments are structured so that pharma loses almost nothing if the drugs fail. The royalties only matter if a drug reaches blockbuster status, which for an AI-designed molecule has never happened.

This ratio is standard across AI drug discovery deals in 2025. Pharma is enthusiastic enough to sign but cautious enough to make nearly all the economics contingent on clinical results that don’t exist yet. The upfront payments fund research. The milestone payments are structured so that pharma loses almost nothing if the drugs fail. The royalties only matter if a drug reaches blockbuster status, which for an AI-designed molecule has never happened.

Novartis expanded its partnership in February 2025, doubling the number of programs to six, targeting what Novartis described as “particularly challenging” and previously undruggable targets, on the same financial terms. That’s a positive signal: it means internal results impressed Novartis scientists enough to commit more targets. The J&J deal, announced January 2026, goes further, covering small molecules, antibodies, peptides, and molecular glues. But “expanded partnerships” and “approved drugs” remain separated by the most unforgiving filter in business: human biology.

Phase II wall

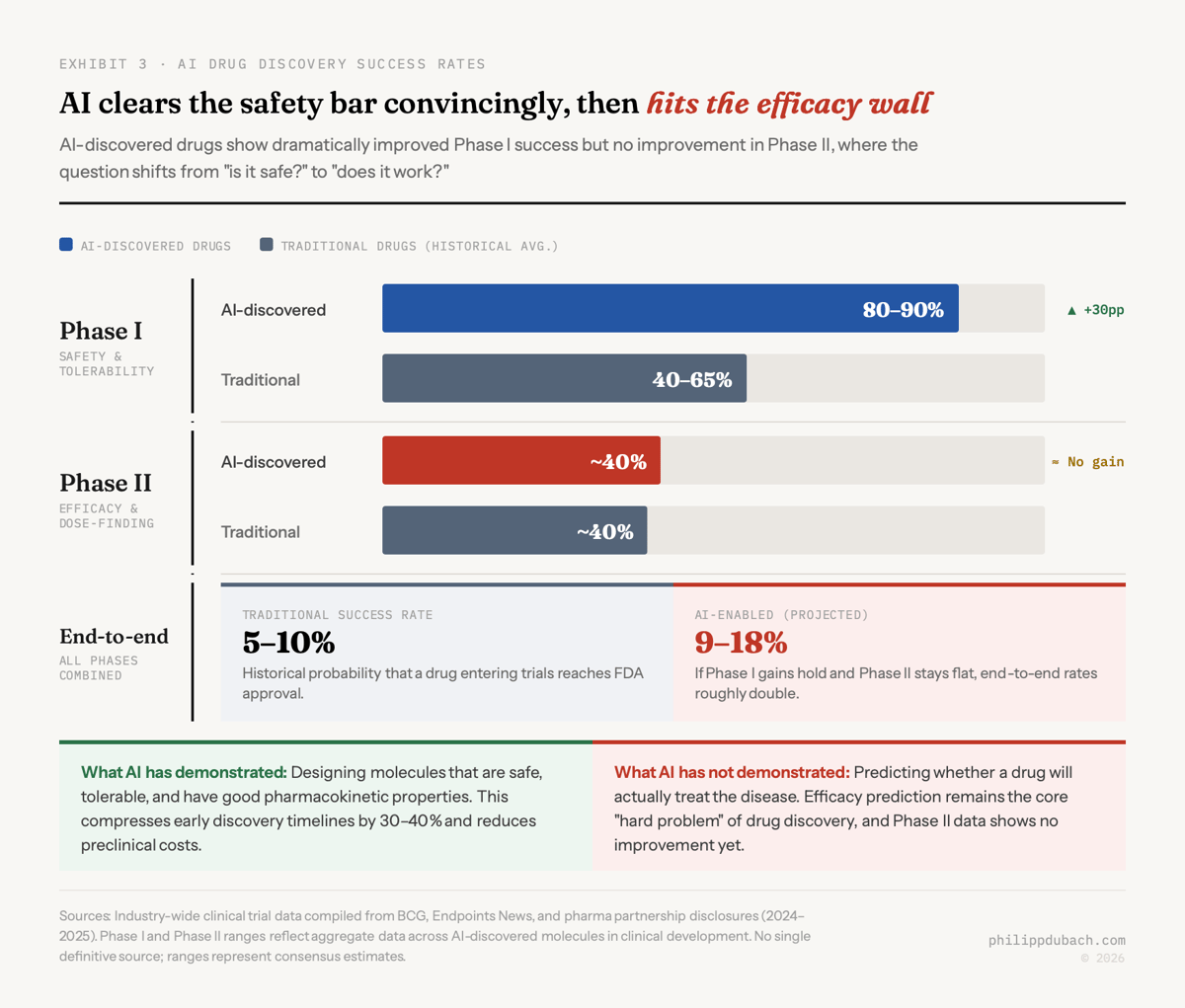

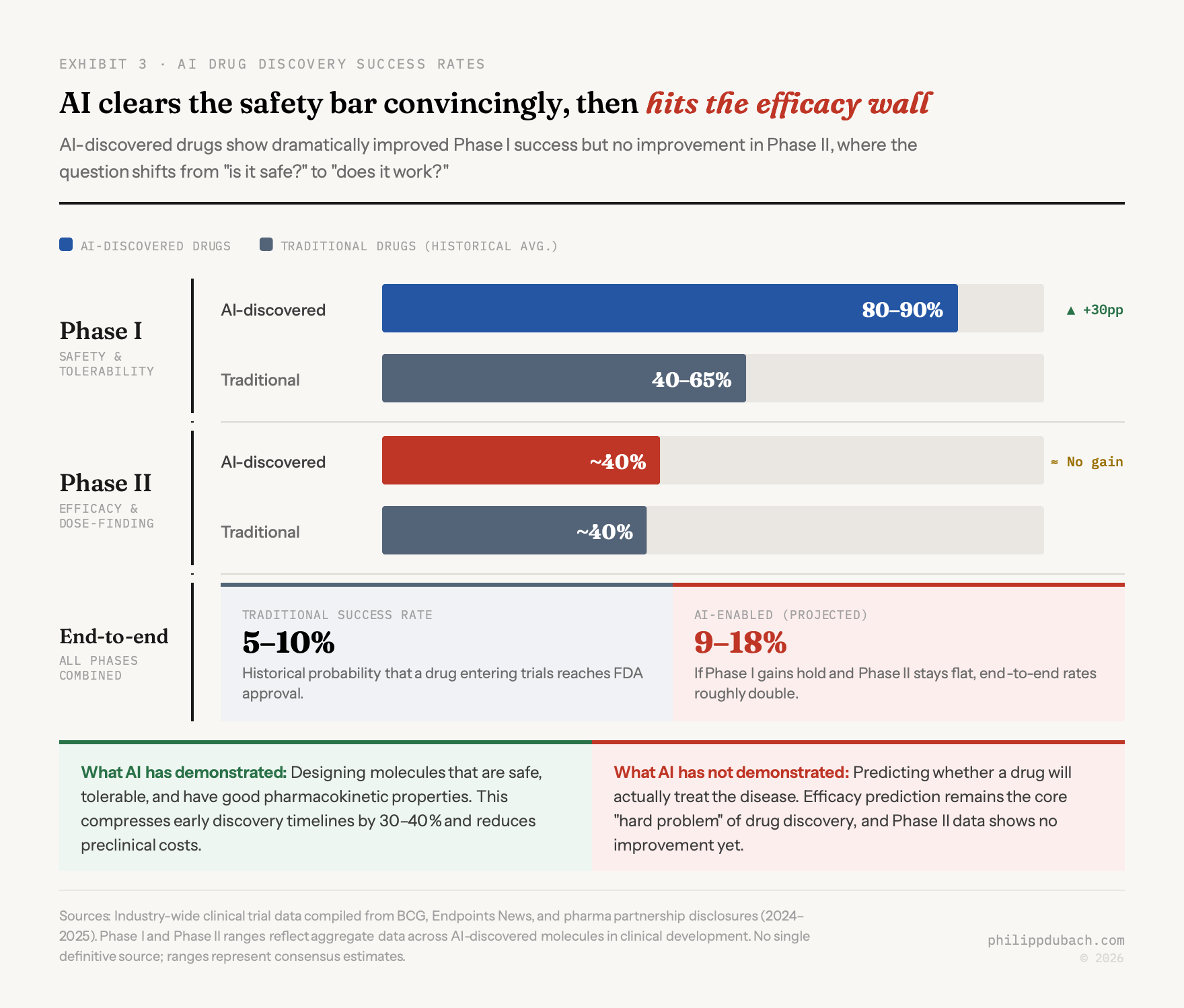

Most commentary on AI drug discovery stops too early. Jayatunga et al. (2024), in the first systematic analysis of AI-discovered drugs in clinical trials, showed AI-discovered molecules achieving 80-90% success rates in Phase I trials, well above the historical 40-65% average. AI is good at designing molecules that are safe and have decent pharmacokinetic properties: they get absorbed, distributed, metabolized, and excreted the way you’d want. Phase I is mostly about safety. AI passes it.

But Phase II is about efficacy. Does the drug actually treat the disease? And here the numbers are sobering: AI-discovered drugs show roughly 40% Phase II success rates, which is about the same as traditionally discovered drugs. AI has not yet demonstrated it can predict whether a molecule will work in a patient, only that it can predict whether a molecule will be tolerable in a patient.

If both trends hold, end-to-end success rates could rise from the historical 5-10% to something like 9-18%. That would roughly double R&D productivity, which in a trillion-dollar industry is worth an enormous amount. McKinsey estimates generative AI could generate $60-110 billion annually in economic value for pharma and medical products. But it’s a far cry from the narrative that generative AI will “solve” drug discovery. It would make drug development somewhat cheaper and faster. An improvement, not a revolution.

If both trends hold, end-to-end success rates could rise from the historical 5-10% to something like 9-18%. That would roughly double R&D productivity, which in a trillion-dollar industry is worth an enormous amount. McKinsey estimates generative AI could generate $60-110 billion annually in economic value for pharma and medical products. But it’s a far cry from the narrative that generative AI will “solve” drug discovery. It would make drug development somewhat cheaper and faster. An improvement, not a revolution.

The counterargument, and it’s a reasonable one, is that IsoDDE represents a qualitative leap that could crack the efficacy problem. Its ability to model induced fits, where proteins reshape to accommodate a drug, and to identify cryptic binding pockets, like the cereblon site that took experimentalists 15 years to find, means it’s capturing biological dynamics that earlier AI systems missed entirely. If better structural understanding translates to better efficacy prediction, the Phase II wall might eventually come down.

I find this plausible but unproven. We’ll know more when Isomorphic’s first candidates enter trials, targeted for late 2026.

Where Isomorphic fits in the competitive stack

Isomorphic’s competitive position is unusual. It leads on computational benchmarks but trails on clinical progress. Insilico Medicine has the most advanced clinical portfolio: its IPF drug ISM001-055 (now called rentosertib) reached Phase IIa with positive results published in Nature Medicine in June 2025, and Insilico has 10+ IND approvals across 31 programs. Recursion Pharmaceuticals, which absorbed Exscientia in a $688 million merger, takes a different approach entirely, running millions of phenomics experiments weekly on 65 petabytes of biological imaging data. Both companies own wet-lab infrastructure that Isomorphic lacks.

What Isomorphic has: the AlphaFold lineage, Alphabet-scale compute, and a unified architecture where each prediction task informs the others. On talent, the company appears to be doing well: 4.7/5 on Glassdoor, 100% CEO approval. They hired Dr. Ben Wolf as CMO in June 2025, formerly at Relay Therapeutics with FDA approval experience for Ayvakit and Gavreto. They opened a Cambridge, Massachusetts office. These are the moves of a company staffing up for clinical reality, not just publishing papers.

The open-source threat is real but manageable in the near term. Chai Discovery (backed by OpenAI at a $1.3 billion valuation, now partnered with Lilly on biologics) and Boltz (partnered with Pfizer) are both making progress. But the gap between IsoDDE’s numbers and the best open-source alternatives is wide enough that Isomorphic has time, maybe 18-24 months, to convert its computational lead into clinical evidence before the field catches up.

Alphabet’s asymmetric position

For Alphabet, Isomorphic is a rounding error that could become a franchise. The Other Bets segment posted a $3.6 billion operating loss in 2025. Alphabet’s net income was $132 billion. The $600 million funding round led by Thrive Capital in March 2025 suggests the company understands the urgency of getting to the clinic, but Alphabet can sustain this bet indefinitely while the underlying science matures, and that patience is itself a competitive advantage most biotech startups don’t have. But does better computation translate to better medicine? IsoDDE’s benchmarks are the best evidence so far that AI can model molecular interactions at this resolution. But Demis Hassabis said it himself:

We know we’re never going to solve drug design with AlphaFold alone. We’ll need half a dozen more breakthroughs of that magnitude.

IsoDDE might be one of those breakthroughs. The clinical data, when it arrives, will tell us whether it’s the kind that matters.