Articles

I Tried Kimi K3 Inside Claude Code

I routed Claude Code through Moonshot AI's Kimi K3, rebuilt a frontend, compared the bill with Claude Opus 4.8 and Fable 5, and sketched what cheap open-weight models could mean for sovereign AI.

Essay 10 min AIAI

Krugman, Fable 5, and Europe in Decline?

US export controls switched off Anthropic's Fable 5 for every non-American. Europe's real decline isn't productivity; it's losing access to frontier AI.

Analysis 7 min AIAI

Midyear Portfolio Review: Valuations got more extreme, not less

Midyear review of the 2026 CHF portfolio through May 29: up 5.2%, roughly matching a 60/40 and trailing the S&P in CHF. Three of four rotations paid; Europe lagged; the clean miss was rates. Plus the three changes I made.

Analysis 10 min InvestingInvesting

How DORA Made Sovereignty a Bank Problem

DORA's 19 Critical ICT Providers list collides with the CLOUD Act and EU Data Act. Sovereignty is now a documented bank deliverable, not a debate.

Analysis 10 min AIAI

Aschenbrenner's Receipts

Aschenbrenner's Situational Awareness committed him to dated AGI predictions. By May 2026 the technology calls landed; the political prescription did not.

Analysis 29 min AIAI

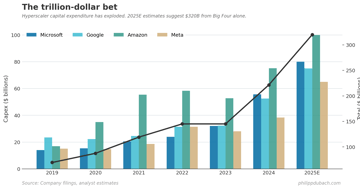

Reconciling Enterprise AI Revenue

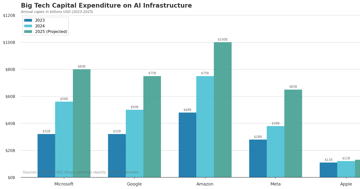

Four enterprise AI revenue figures span a 40x range. The $63.2B audit-grade floor is the only tier that defensibly underwrites $690B of hyperscaler capex.

Analysis 13 min AIAI

What Claude Thinks But Doesn't Say

Anthropic's natural language autoencoders translate Claude's activations into readable text. The method works. The press release skips three structural problems.

Commentary 12 min AIAI

Two Anthropics

Two Anthropics: the safety lab Dario founded in 2021 and the $380B frontier lab it became. Same organism, two narratives the company itself has to reconcile. Three scenarios for how the tension resolves.

Commentary 12 min AIAI

Karpathy's Software 3.0 Playbook

Twelve lessons from Andrej Karpathy's Sequoia interview: Software 3.0, vibe coding versus agentic engineering, jagged intelligence, and why December 2024 was the inflection most people missed.

Commentary 10 min AIAI

Inside PRAGMA: Revolut's Foundation Model for Banking

Revolut's PRAGMA is a 1B-parameter encoder trained on 24B banking events. Reading the paper, comparing with Nubank's nuFormer, planning a rebuild.

Analysis 6 min AIAI

The Moral Philosophy of Investing in Ignorance

Constraint arbitrage, the sidecar problem, and who bears the distributional cost of investing under ignorance. The final installment of Edge of Knowledge.

Analysis 8 min Quantitative FinanceQuant

Bet Sizing at the Frontier

The Kelly Criterion assumes you know your probability of winning. In a UU world, you don't, and heuristics like Zeckhauser's Maxim B replace false precision.

Analysis 9 min Quantitative FinanceQuant

The Geometry of Who Knows What

When neither side can define the states of the world, adverse selection fears are misplaced. Zeckhauser's information matrices and constraint arbitrage.

Analysis 9 min Quantitative FinanceQuant

Do Not Disturb My Circles

AlphaFold cost under $1M to train. OpenAI spends $2.3B on inference. The chatbot era consumed the talent and compute that could have cured diseases.

Commentary 13 min AIAI

Why Lilly's Weight Loss Pill Isn't a Peptide

Oral semaglutide destroys 99% of its active ingredient per dose. Lilly's Foundayo skips the problem entirely. Inside the $70B oral GLP-1 pill race.

Analysis 9 min MedicineMedicine

Ambiguity by Design

Ellsberg proved people flee unknown odds. Zeckhauser showed their flight creates mispricing. Part 2 on ambiguity aversion, comparative ignorance, and investing.

Analysis 8 min Quantitative FinanceQuant

Three Kinds of Not-Knowing

Knightian uncertainty splits not-knowing into risk, uncertainty, and ignorance. A century after Knight and Keynes, most of investing still ignores the split.

Analysis 9 min Quantitative FinanceQuant

On-Device AI Models Will Be The New Reason to Upgrade Your Phone

Smartphones haven't had a compelling upgrade story in years. On-device AI models, distilled from frontier systems like Gemini, are about to change that. Parameters are the new megapixels.

Commentary 5 min AIAI

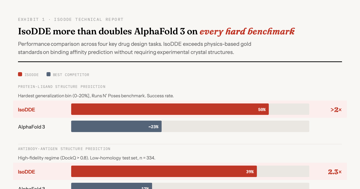

AI Can Now Design Drugs in Seconds; We Still Can't Tell You If They Work.

IsoDDE doubles AlphaFold 3 on hard benchmarks and beats physics-based gold standards. But no AI drug has FDA approval. What $4B in pharma deals actually mean.

Essay 6 min MedicineMedicine

The Last Architecture Designed by Hand

The transformer's limits are now mathematical proofs, not empirical hunches. Hybrids are in production. AI is searching for its own replacement. Here's what comes after.

Analysis 6 min AIAI

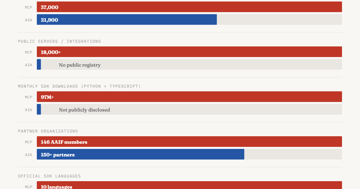

MCP vs A2A in 2026: How the AI Protocol War Ends

MCP leads with 97M monthly SDK downloads and 10,000+ servers. A2A fills a different layer. Analysis of the agentic AI standards war with historical parallels.

Analysis 8 min AIAI

AI Models Are the New Rebar

Qwen 3.5-35B runs on a gaming PC and matches Claude Sonnet 4.5. When the commodity version is 95% as good and 97% cheaper, you have a pricing problem.

Analysis 8 min AIAI

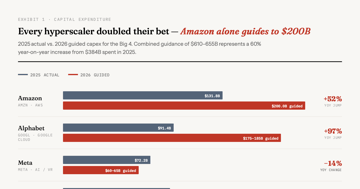

AI Capex Arms Race: Who Blinks First?

Alphabet's free cash flow is on track to fall 90% in 2026. Amazon's is at $11B. $690B in AI capex is cannibalizing the cash that justified these valuations.

Analysis 8 min InvestingInvesting

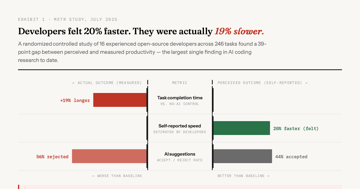

93% of Developers Use AI Coding Tools. Productivity Hasn't Moved.

METR found experienced developers 19% slower with AI, despite feeling 20% faster. At 92.6% adoption, organizational productivity gains remain roughly 10%.

Analysis 9 min TechTech

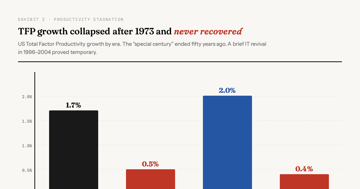

The Physics Department That Slowed Down

Peter Thiel says physics stalled in 1972. Then GPT-5.2 proved a new result in theoretical physics. The 75:1 AI compute gap between commerce and science.

Essay 8 min AIAI

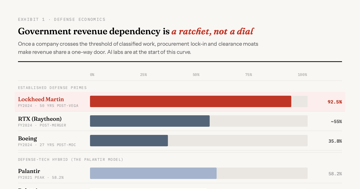

When AI Labs Become Defense Contractors

The Anthropic-Pentagon standoff isn't an ethics story. It's a replay of the 1993 Last Supper that consolidated 51 defense primes into 5, at Silicon Valley speed.

Analysis 8 min AIAI

Every Bulge Bracket Bank Agrees on AI

I read 12 AI research reports from Goldman Sachs, JPMorgan, UBS, and 6 other banks. Here's the consensus they're pushing, and what they're not saying.

Analysis 10 min AIAI

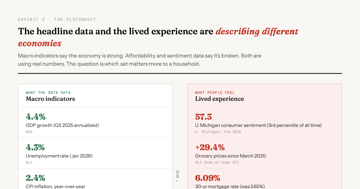

People Live in Levels, Not Rates

Prices rose 25% since 2020 and won't come back. The levels-vs-rates problem explains the vibecession, the Stewart-Thaler debate, and why nobody trusts economists.

Commentary 7 min MacroMacro

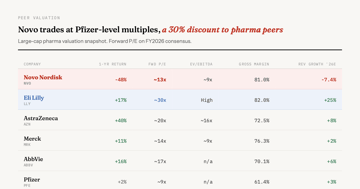

Novo Was Europe's Most Valuable Company

Novo Nordisk lost 75% since June 2024. CagriSema failed vs Zepbound, US pricing is resetting lower, and Lilly leads on every axis. Full breakdown with numbers.

Analysis 9 min MedicineMedicine

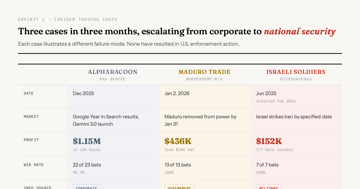

The Absolute Insider Mess of Prediction Markets

A Google insider made $1.15M on Polymarket in 24 hours. Israeli soldiers bet classified strike timing. Why prediction markets need insider trading regulation.

Analysis 12 min InvestingInvesting

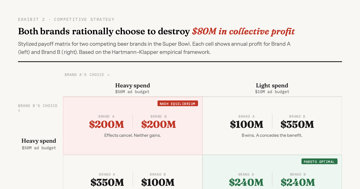

Economics of a Super Bowl Ad

A 30-second Super Bowl spot costs $8M. The real price is $16–23M. The ROI evidence is mixed. A deep look at the pricing, the prisoner's dilemma, and the NFL.

Analysis 11 min EconomicsEconomics

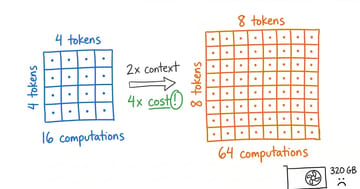

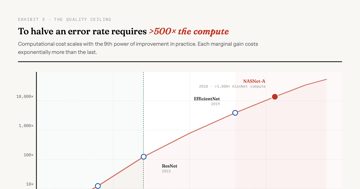

The Impossible Backhand

AI converges to the mean by design. Ninth-power scaling costs and a 53-point gap on Humanity's Last Exam show domain expertise is appreciating, not declining.

Essay 10 min AIAI

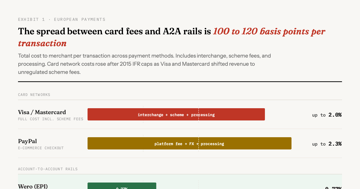

Europe's $24 Trillion Payment Breakup Is Really a Bet on Infrastructure Arbitrage

The EuroPA alliance connected 130 million users across 13 countries overnight. But this isn't really about sovereignty. It's an infrastructure arbitrage exploiting a 100-120bps spread between card network fees and SEPA Instant rails, accidentally protected by the EU's own regulation.

Essay 14 min MacroMacro

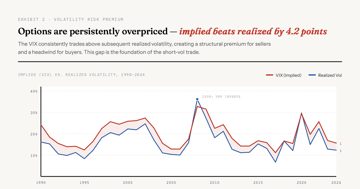

Long Volatility Premium

One River's data shows beta-adjusted long volatility outperformed the S&P 500 over 40 years. Goldman, AQR, and Universa agree on the mechanism but disagree on implementation. A synthesis of the evidence.

Essay 12 min Quantitative FinanceQuant

The SaaSpocalypse Paradox

AI capex failure and AI replacing all software are mutually exclusive. Why the 2026 SaaSpocalypse is a $2 trillion pricing error, not an extinction event.

Essay 8 min AIAI

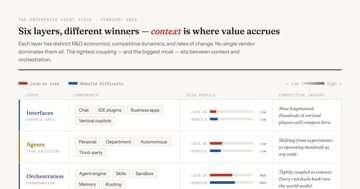

Don't Go Monolithic; The Agent Stack Is Stratifying

The enterprise AI agent stack is stratifying into six layers with different winners at each. Models commoditize; context — your organizational world model — compounds. A framework for agentic AI architecture decisions.

Essay 8 min AIAI

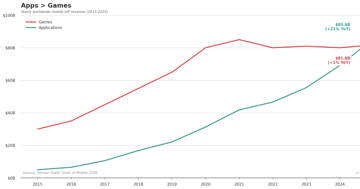

Where Mobile Money Goes Now

Apps overtook games in mobile IAP revenue for the first time in 2025, driven by $3.5B in GenAI growth. Analysis of Sensor Tower's State of Mobile 2026 report.

Analysis 3 min AIAI

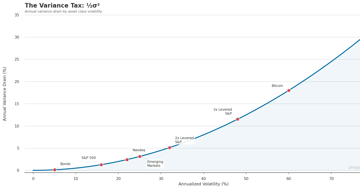

Variance Tax

Variance drain is the hidden cost of volatility: why a portfolio averaging +10% can lose money. The ½σ² formula explains the gap between paper and real returns.

Essay 4 min Quantitative FinanceQuant

Claude Opus 4.6: Anthropic's New Flagship AI Model for Agentic Coding

Claude Opus 4.6 brings a 1M token context window, 68.8% ARC-AGI-2, and Agent Teams to Claude Code. Full benchmark comparison vs GPT-5.2 and Gemini 3 Pro with pricing analysis.

Commentary 6 min AIAI

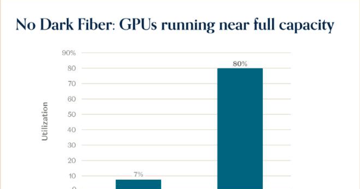

Buying the Haystack Might Not Work This Year

a16z sees AI fundamentals thriving with 80% GPU utilization. AQR sees the CAPE at the 96th percentile. Both have data. Both may be right.

Commentary 4 min AIAI

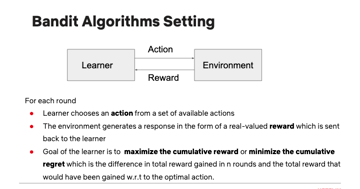

Bandits and Agents: Netflix and Spotify Recommender Stacks in 2026

How hybrid recommender systems balance multi-armed bandits against LLM inference cost economics in 2026. A deep dive into Netflix recommendation algorithm architecture and Spotify's AI DJ recommender system.

Essay 5 min AIAI

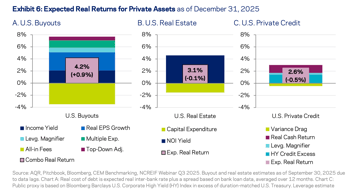

Is Private Equity Just Beta With a Lockup?

AQR's 2026 data shows private equity returning 4.2% versus 3.9% for public equities. The 30bp illiquidity premium barely justifies years of lockup.

Commentary 4 min Quantitative FinanceQuant

Britain's Strategic Limbo

Britain faces strategic isolation: locked out of EU defense cooperation, unwilling to join Trump's coalition. The mid-Atlantic bridge has nowhere to land.

Analysis 3 min MacroMacro

The Rise of Middle Power Realism

At Davos 2026, Carney told allies to take down the signs of the liberal order. Middle powers are learning to navigate between giants without illusions.

Analysis 4 min MacroMacro

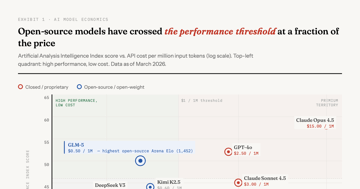

The Most Expensive Assumption in AI

Sara Hooker's research challenges the trillion-dollar scaling thesis. Compact models now outperform massive ones as diminishing returns hit AI.

Commentary 4 min AIAI

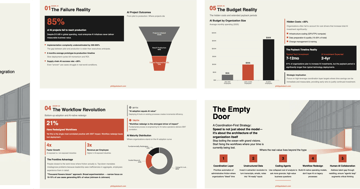

Enterprise AI Strategy is Backwards

85% of AI projects fail. Only 26% translate pilots to production. The winners automate the coordination layer where employees spend 57% of their workday.

Essay 2 min AIAI

Big in Japan

Japan holds $5 trillion in foreign assets. With 30-year JGB yields now above 3%, the carry trade that defined Japanese investing faces new friction.

Commentary 2 min MacroMacro

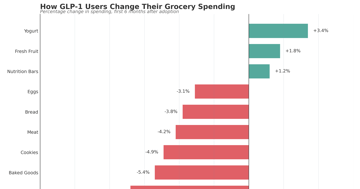

Ozempic is Reshaping the Fast Food Industry

Cornell research: GLP-1 users cut grocery spending 5.3%, fast food 8%. With 16% household adoption and savory snacks down 10%, food stocks face headwinds.

Commentary 4 min MedicineMedicine

Does AI mean the demand on labor goes up?

AI was supposed to free us. The Jevons paradox plays out in real time: efficiency expands workload, not leisure. 77% of workers say AI added to their work.

Commentary 2 min AIAI

Repo might be even bigger than we thought

New OFR data reveals $12.6 trillion in daily repo exposures—$700 billion larger than previous estimates. The plumbing of modern money remains poorly understood.

Commentary 5 min MacroMacro

The Market Can Stay Irrational Longer Than You Can Stay Solvent

Steve Eisman explains how U.S. equity markets have structurally decoupled from everyday economic reality through concentration and passive investing.

Commentary 4 min InvestingInvesting

Beyond Vector Search: Why LLMs Need Episodic Memory

Context windows aren't memory. Explore EM-LLM's episodic architecture, knowledge graph tools like Mem0 and Letta, and why vectors fail for sequential data.

Essay 3 min AIAI

Praise by Name, Criticize by Category: Warren Buffett Retires at 95

Buffett exits after paying $26.8B in taxes. What 60 years of letters reveal about admitting mistakes, insurance float, and why Abel inherits $300B in cash.

Essay 5 min InvestingInvesting

Apple's AI Bet: Playing the Long Game or Missing the Moment?

Apple's $157B cash pile and Gemini-powered Siri shift show a restrained AI strategy. Analysis of whether Apple wins as AI models become commodities.

Commentary 3 min AIAI

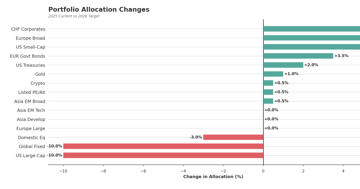

How AI is Shaping My Investment Portfolio for 2026

Rebalancing for 2026: reducing S&P 500 at 40× CAPE, adding Europe after Germany's €1T pivot, and bonds at 4.2% yields. Full allocation rationale.

Essay 10 min InvestingInvesting

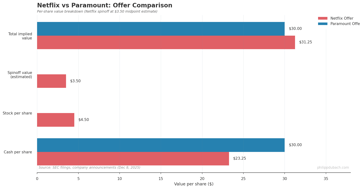

Not Logan Roy: Netflix vs. Paramount's Bidding War

Netflix's $72B Warner Bros deal vs Paramount's hostile $30/share tender. Deal mechanics, aggregation theory, and why internet distributors win streaming.

Analysis 7 min InvestingInvesting

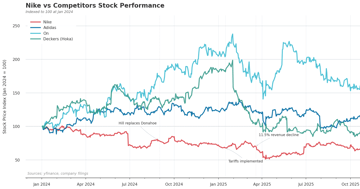

Nike's Crisis and the Economics of Brand Decay

Nike lost $28B by weakening product development, athlete partnerships, and marketing simultaneously. Data-driven analysis of how complementary assets collapse.

Analysis 8 min InvestingInvesting

Michael Burry's $379 Newsletter

Michael Burry launches Substack warning AI markets mirror 1999. His Nvidia-Cisco comparison, the GPU depreciation debate, and what hyperscalers need to justify capex.

Commentary 5 min InvestingInvesting![Is AI Really Eating the World? AGI, Networks, Value [2/2] — AGI predictions miss the point. Multiple competing models means price war. Value …](https://static.philippdubach.com/cdn-cgi/image/fit=crop,gravity=right,width=360,height=189,quality=80,format=auto/ograph/ograph-eatingtheworld2.jpg)

Is AI Really Eating the World? AGI, Networks, Value [2/2]

AGI predictions miss the point. Multiple competing models means price war. Value flows to applications, customer relationships, and vertical integrators.

Essay 7 min AIAI![Is AI Really Eating the World? [1/2] — Hyperscalers spend $400B on AI, API prices drop 97%, and DeepSeek builds …](https://static.philippdubach.com/cdn-cgi/image/fit=crop,gravity=right,width=360,height=189,quality=80,format=auto/ograph/ograph-eatingtheworld1.jpg)

Is AI Really Eating the World? [1/2]

Hyperscalers spend $400B on AI, API prices drop 97%, and DeepSeek builds frontier models for $500M. Value is flowing to applications, not model providers.

Analysis 5 min AIAI

Weather Forecasts Have Improved a Lot

Four-day forecasts now match one-day accuracy from 30 years ago. How AI models like WeatherNext 2 use CRPS training to preserve extreme weather signals.

Analysis 2 min AIAI

GLP-1 Receptor Agonists in ASUD Treatment

A phase 2 RCT shows low-dose semaglutide reduces alcohol craving and heavy drinking with effect sizes exceeding naltrexone. What GLP-1 means for AUD treatment.

Commentary 2 min MedicineMedicine

AI Models as Standalone P&Ls

OpenAI lost $11.5B in one quarter. But Anthropic CEO Dario Amodei argues each AI model is independently profitable. Here's why the math is complicated.

Commentary 5 min AIAI

Working with Models

Diffusion models corrupt data into noise, then reverse the process. Learn the math with Stefano Ermon's Stanford CS236 course, free on YouTube.

Commentary 1 min AIAI![Pozsar's Bretton Woods III: Three Years Later [2/2] — Gold above $4,000, Treasury holdings below $7T, but the dollar still dominates …](https://static.philippdubach.com/cdn-cgi/image/fit=crop,gravity=right,width=360,height=189,quality=80,format=auto/ograph/ograph-Pozsar2.jpg)

Pozsar's Bretton Woods III: Three Years Later [2/2]

Gold above $4,000, Treasury holdings below $7T, but the dollar still dominates 88% of FX volumes. What Pozsar's Bretton Woods III got right and wrong.

Analysis 6 min MacroMacro![Pozsar's Bretton Woods III: The Framework [1/2] — How freezing Russian reserves sparked Bretton Woods III: Pozsar's framework on …](https://static.philippdubach.com/cdn-cgi/image/fit=crop,gravity=right,width=360,height=189,quality=80,format=auto/ograph/ograph-Pozsar1.jpg)

Pozsar's Bretton Woods III: The Framework [1/2]

How freezing Russian reserves sparked Bretton Woods III: Pozsar's framework on inside money, outside money, and the shift to a commodity-backed monetary order.

Analysis 7 min MacroMacro

Everything is a DCF Model

Michael Mauboussin's argument that every cash-generating asset is valued through a DCF model. Why this Morgan Stanley paper changed how I think about value.

Commentary 1 min InvestingInvesting

Agent-based Systems for Modeling Wealth Distribution

Agent-based modeling shows how random market transactions naturally produce extreme wealth concentration, and why even a small wealth tax changes everything.

Analysis 2 min EconomicsEconomics

Novo Nordisk's Post-Patent Strategy

Novo Nordisk's lead replacement candidate amycretin reported Phase 1 data in The Lancet. How the company is positioning around the 2031 Ozempic patent cliff.

Commentary 4 min MedicineMedicineAbout these essays

- What does Philipp Dubach write about?

- Long-form essays, analyses, and notes on quantitative finance, AI, and technology. Independent research-style writing — not commentary, not aggregation. Some essays are formalized as peer-reviewed papers and pre-prints with DOIs on SSRN and arXiv.

- How often are essays published?

- There is no fixed schedule. Essays appear when an idea is worth writing up, typically a few times a month. Subscribers receive new essays by email; the RSS and JSON feeds carry the same content.

- Where can I find the source code or papers behind these essays?

- Essays that ship with code link to public GitHub repositories inline. Peer-reviewed papers and pre-prints are listed on the Research page with DOI links to SSRN and arXiv. Builds and reproducible projects are catalogued on the Projects page.