Novo Nordisk was Europe’s most valuable company 20 months ago. Today its market capitalization falls behind ASML, LVMH, Hermès, L’Oréal, SAP, Prosus, Siemens, Inditex, Deutsche Telekom, and Santander.

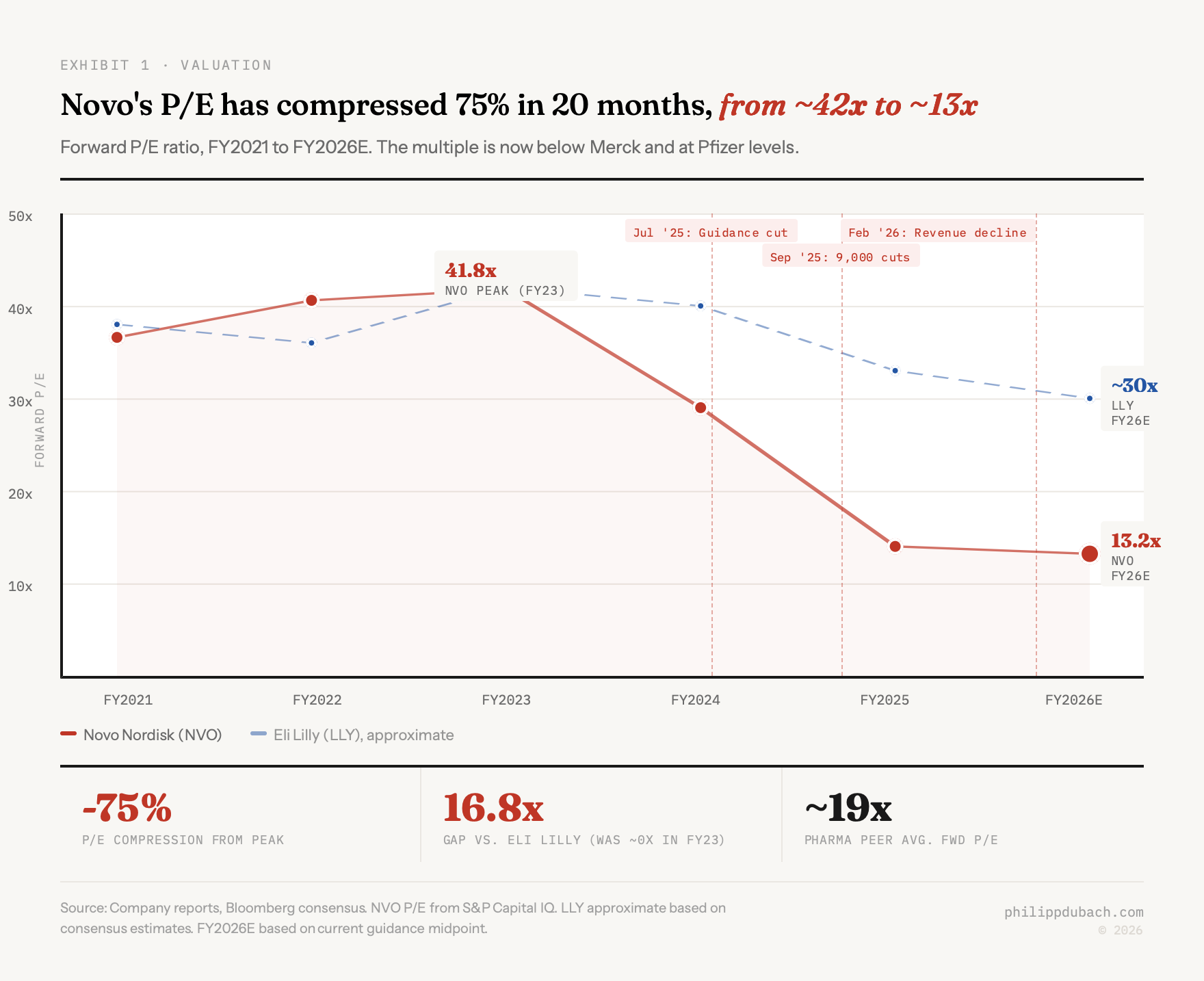

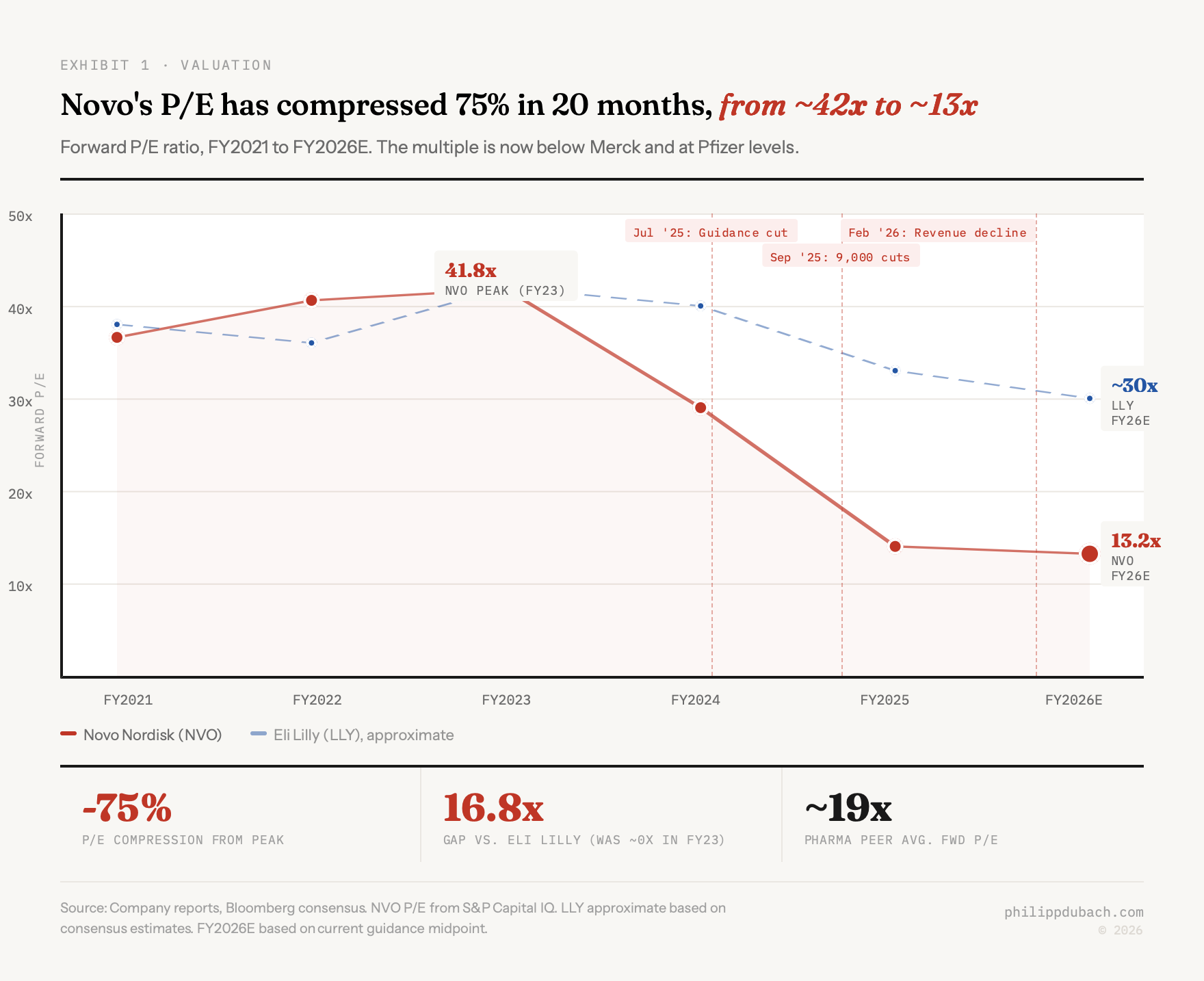

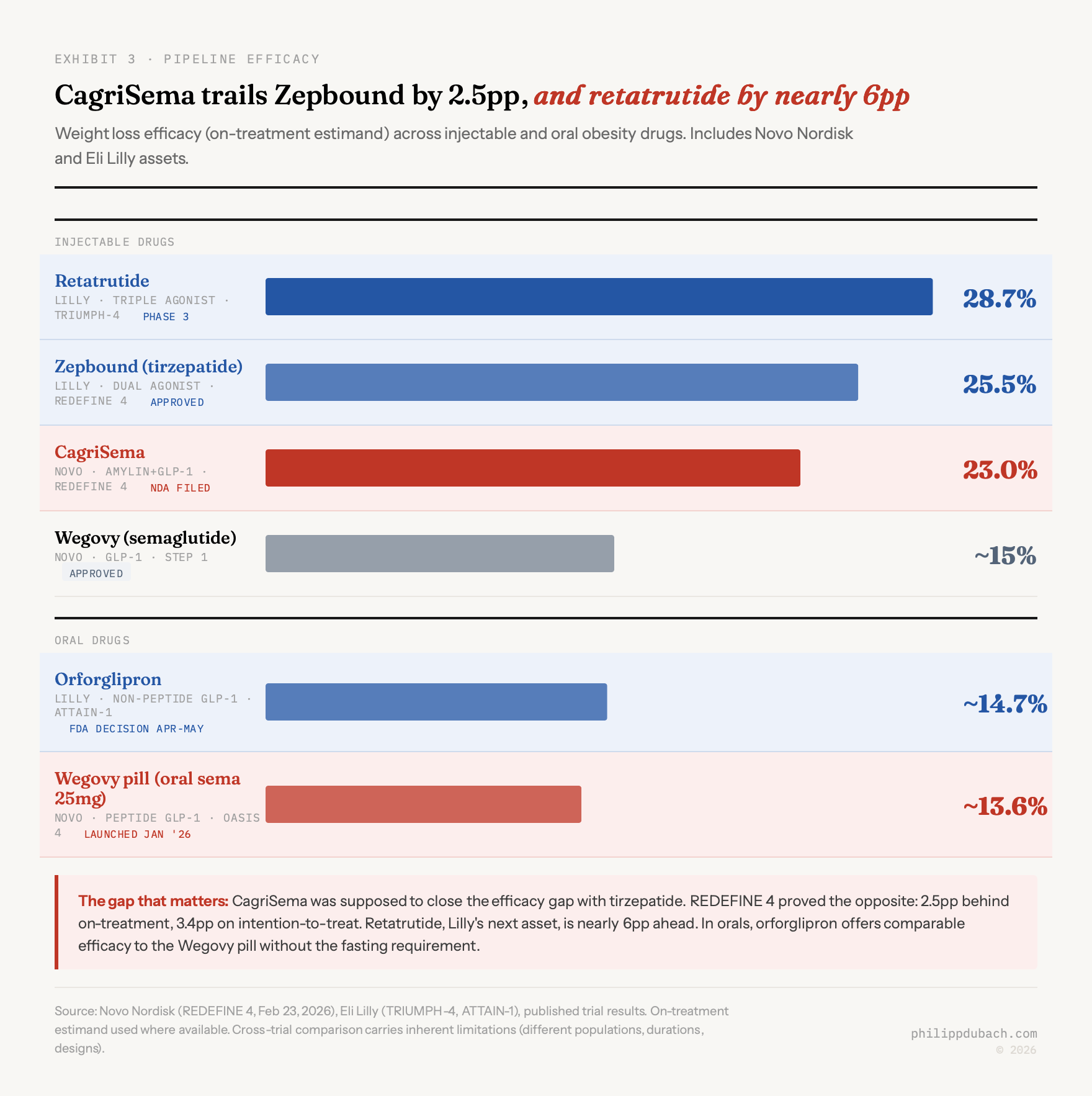

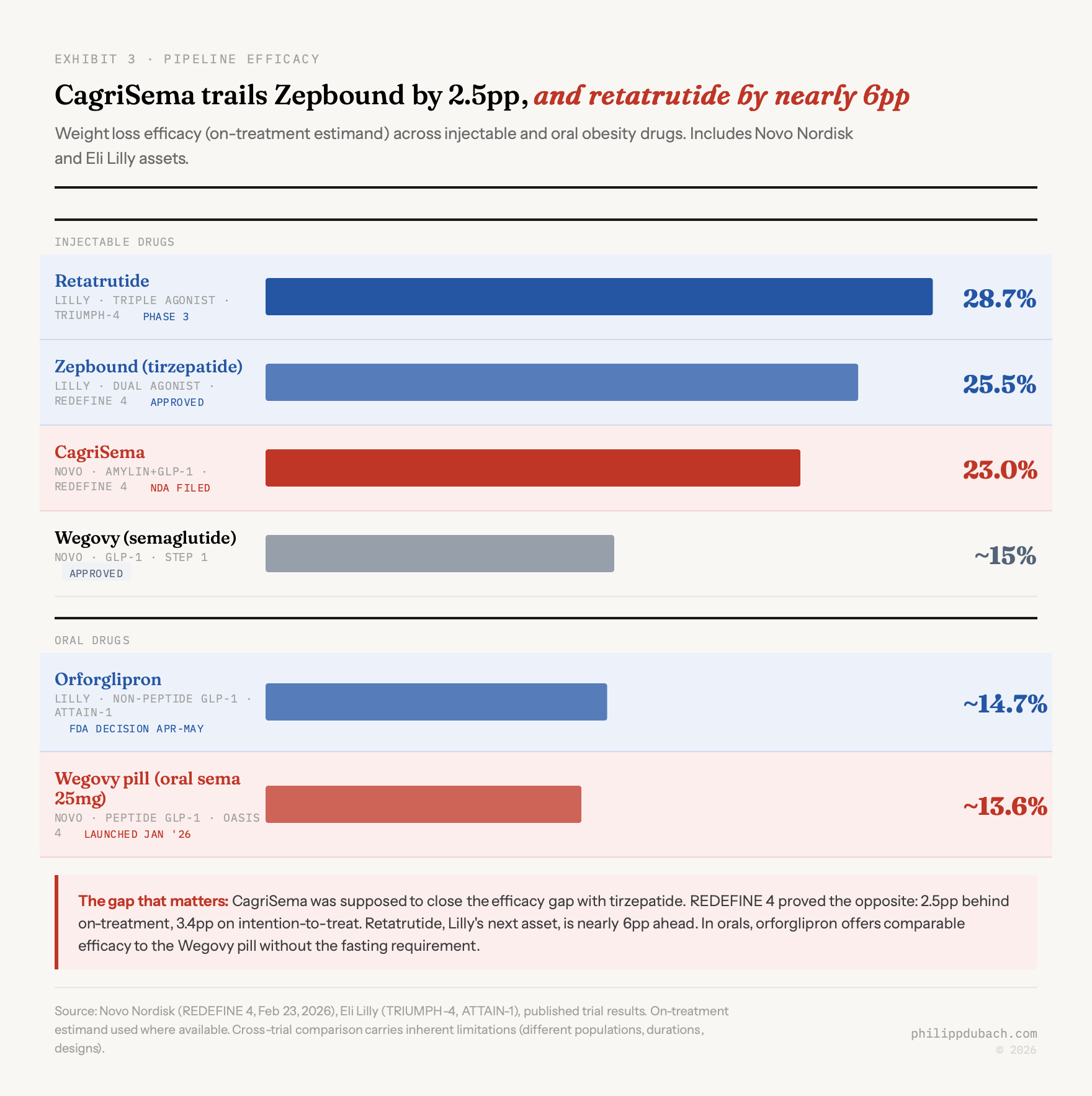

The stock has lost roughly 75% since its June 2024 peak of $142.44, falling from a $640 billion market cap to under $160 billion. Shares dropped another 16% this morning after CagriSema, the follow-on obesity drug that was supposed to restore Novo’s competitive story, failed its head-to-head trial against Eli Lilly’s Zepbound. The REDEFINE 4 results confirm what a former Novo advisor told AlphaSense back in December: CagriSema is “not particularly impressive.”

I like this stock over the long term. The GLP-1 market is real, the addressable population is enormous, and Novo still sells more semaglutide than anyone. But liking a stock and holding on to it no matter the outlook are not the same thing. Or as Warren Buffett would say:

The most important thing to do if you find yourself in a hole is to stop digging

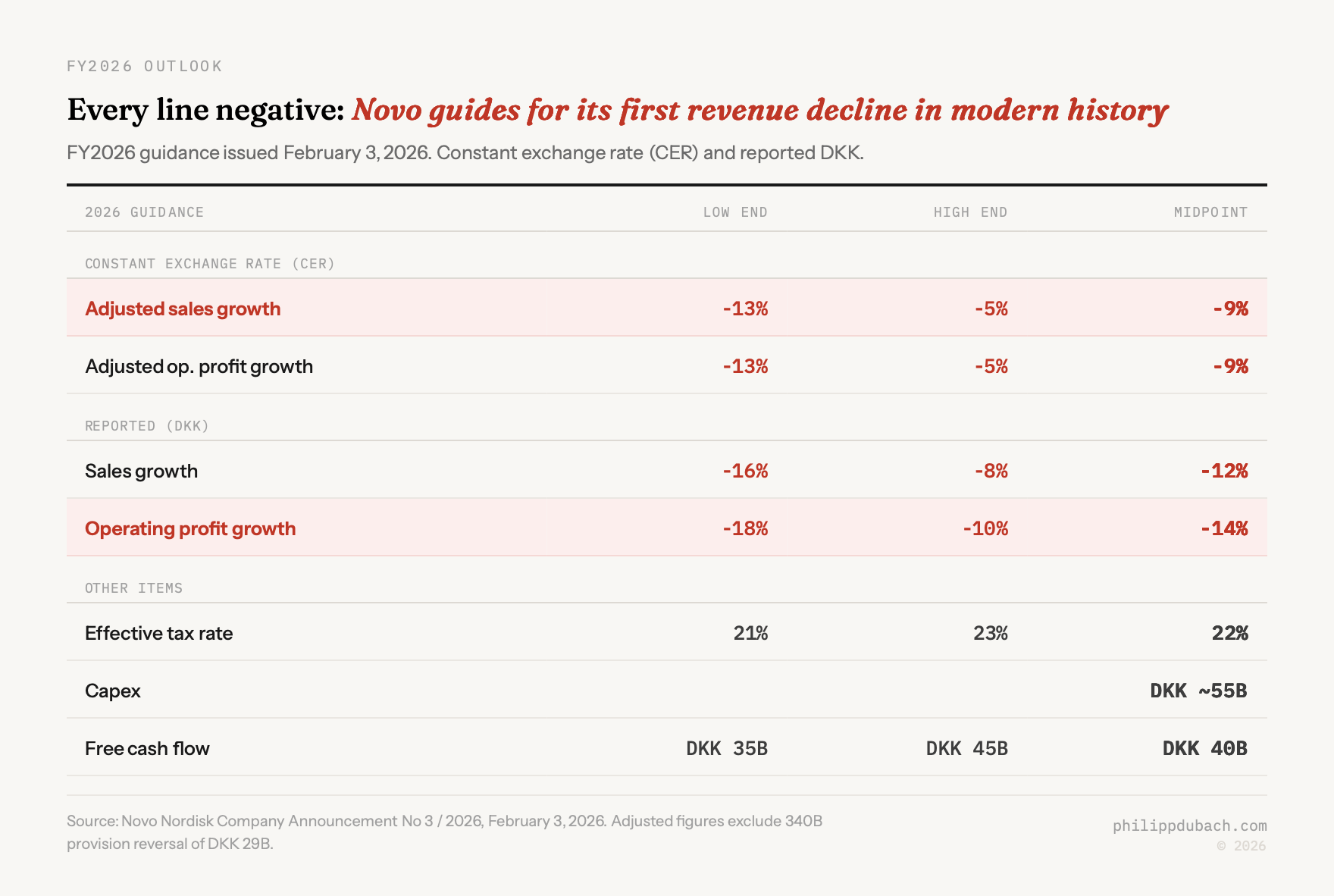

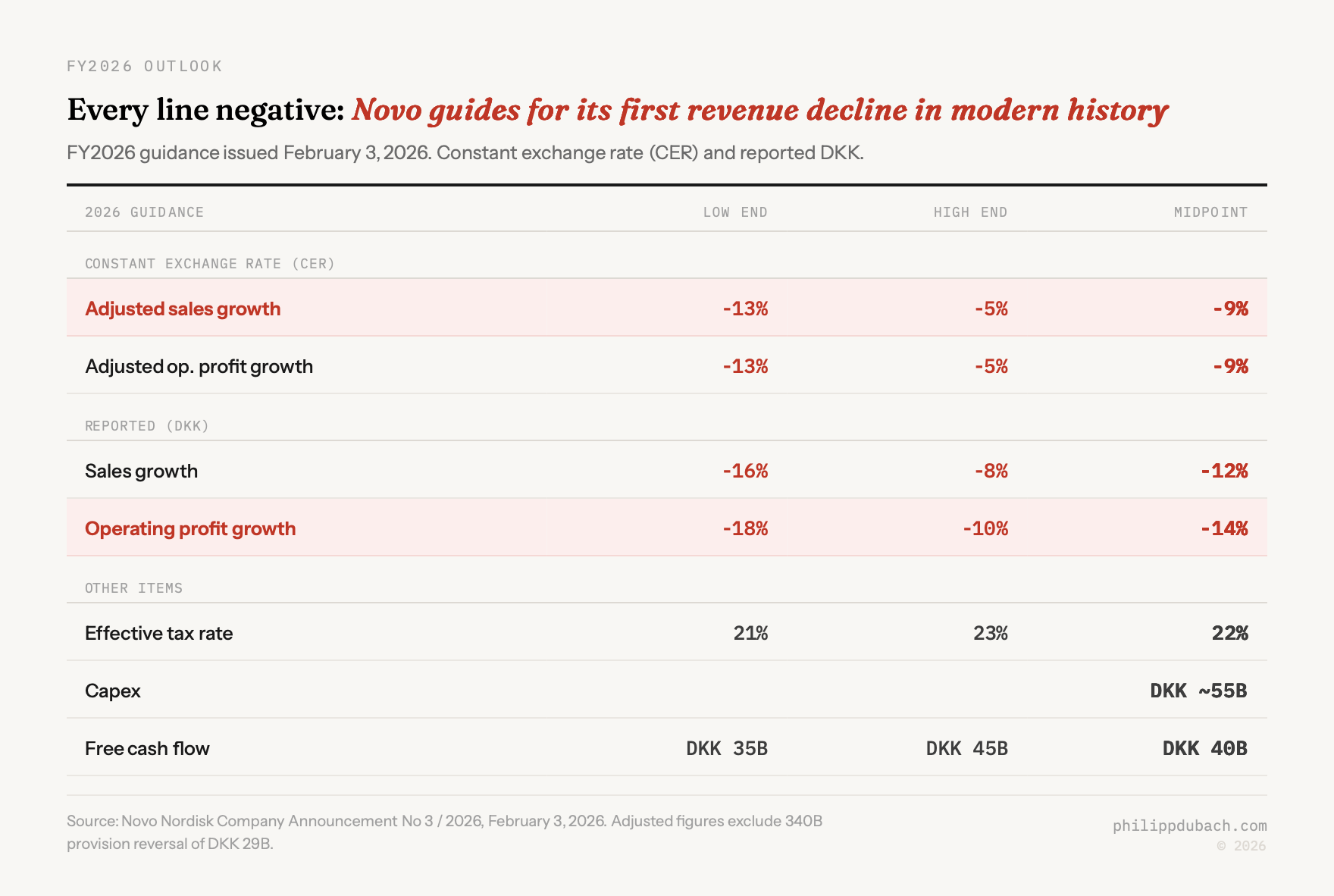

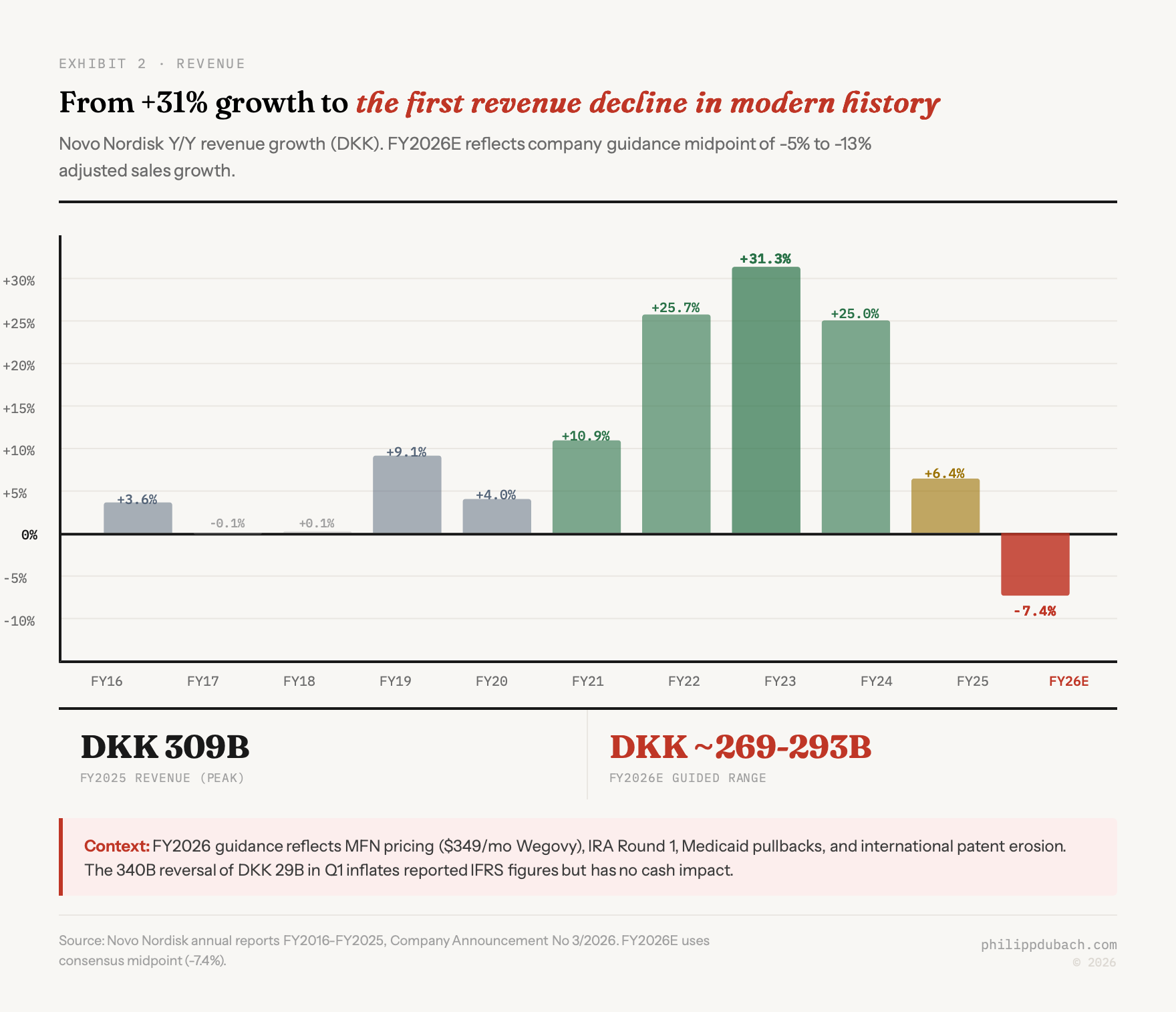

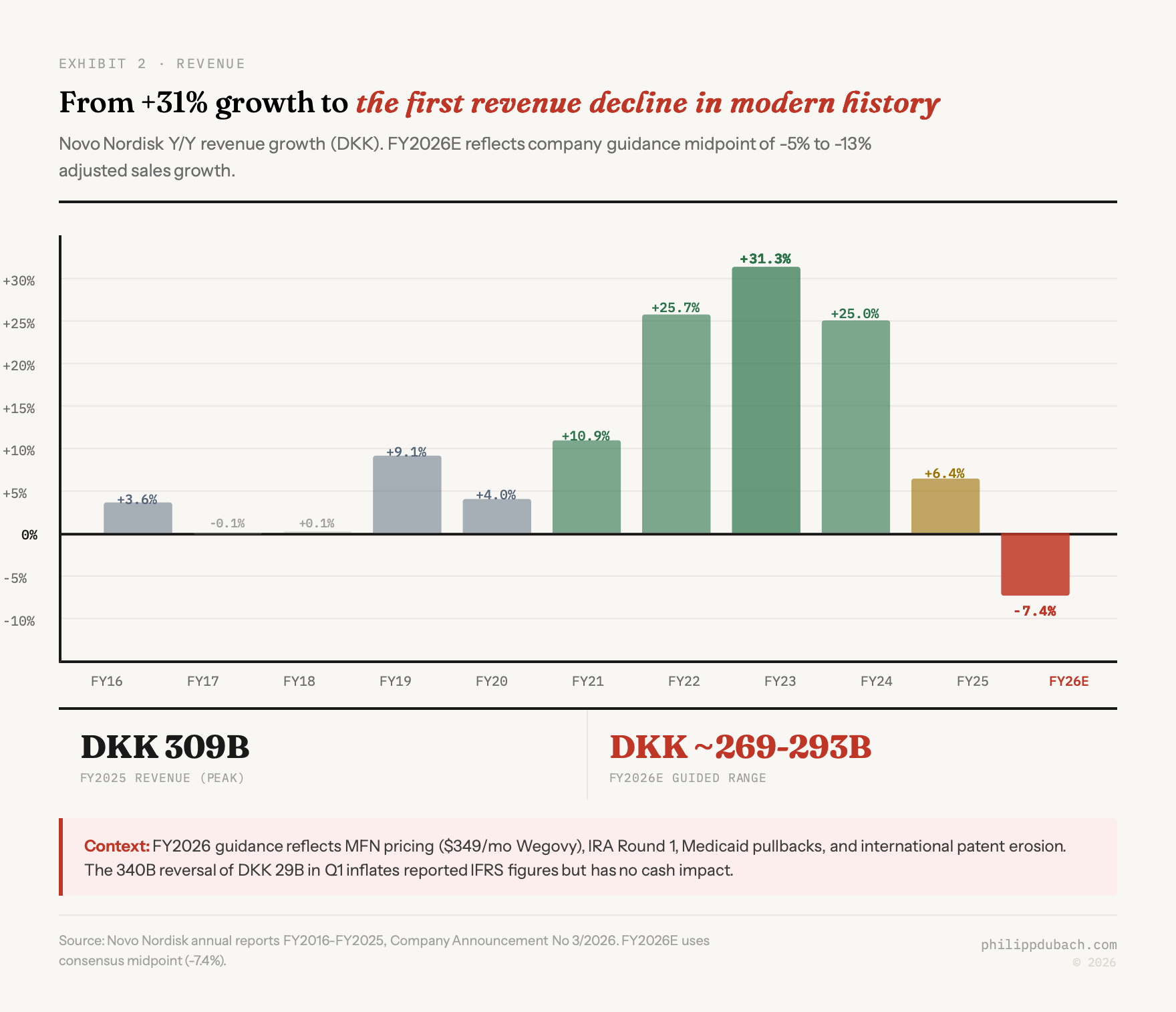

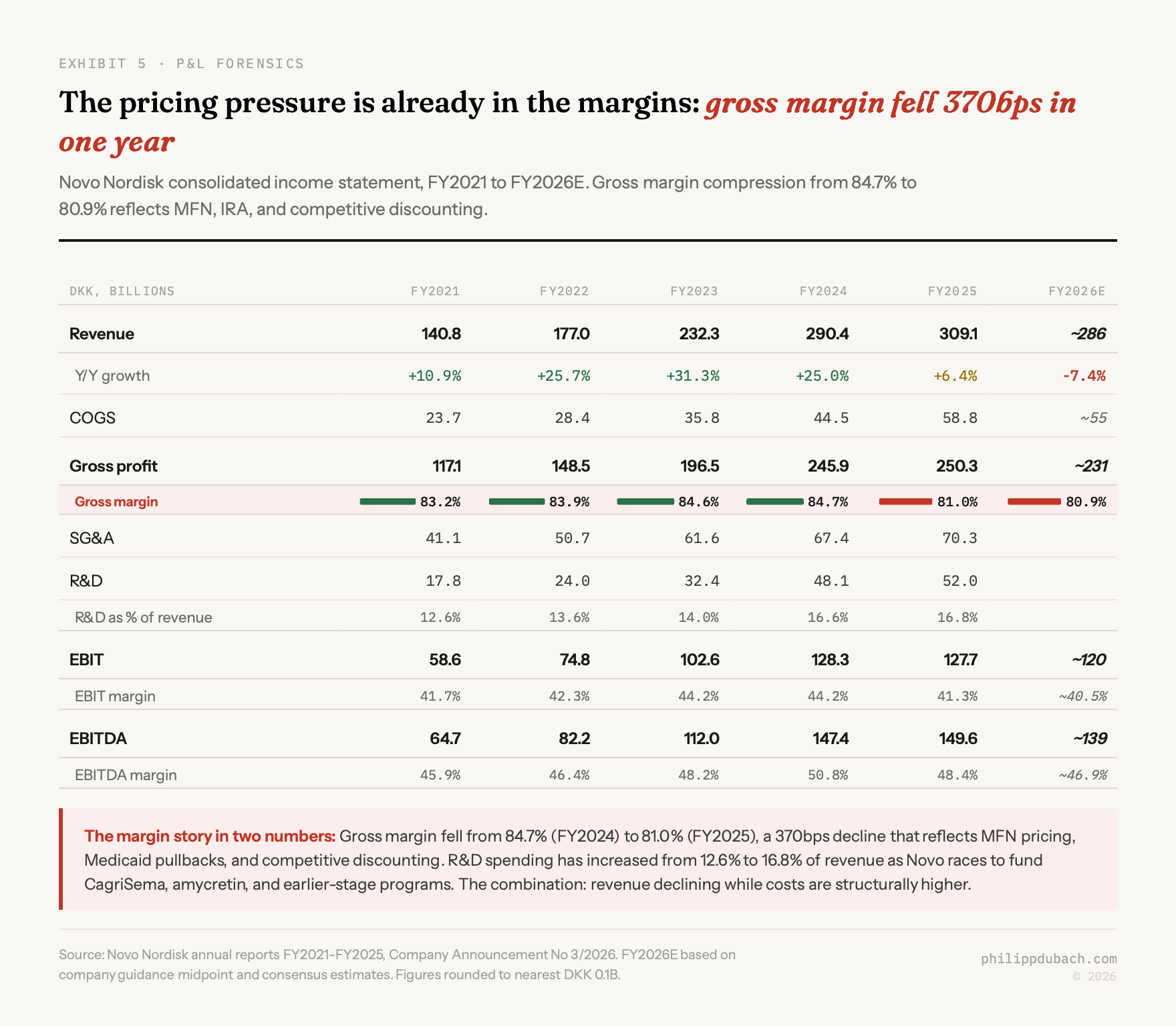

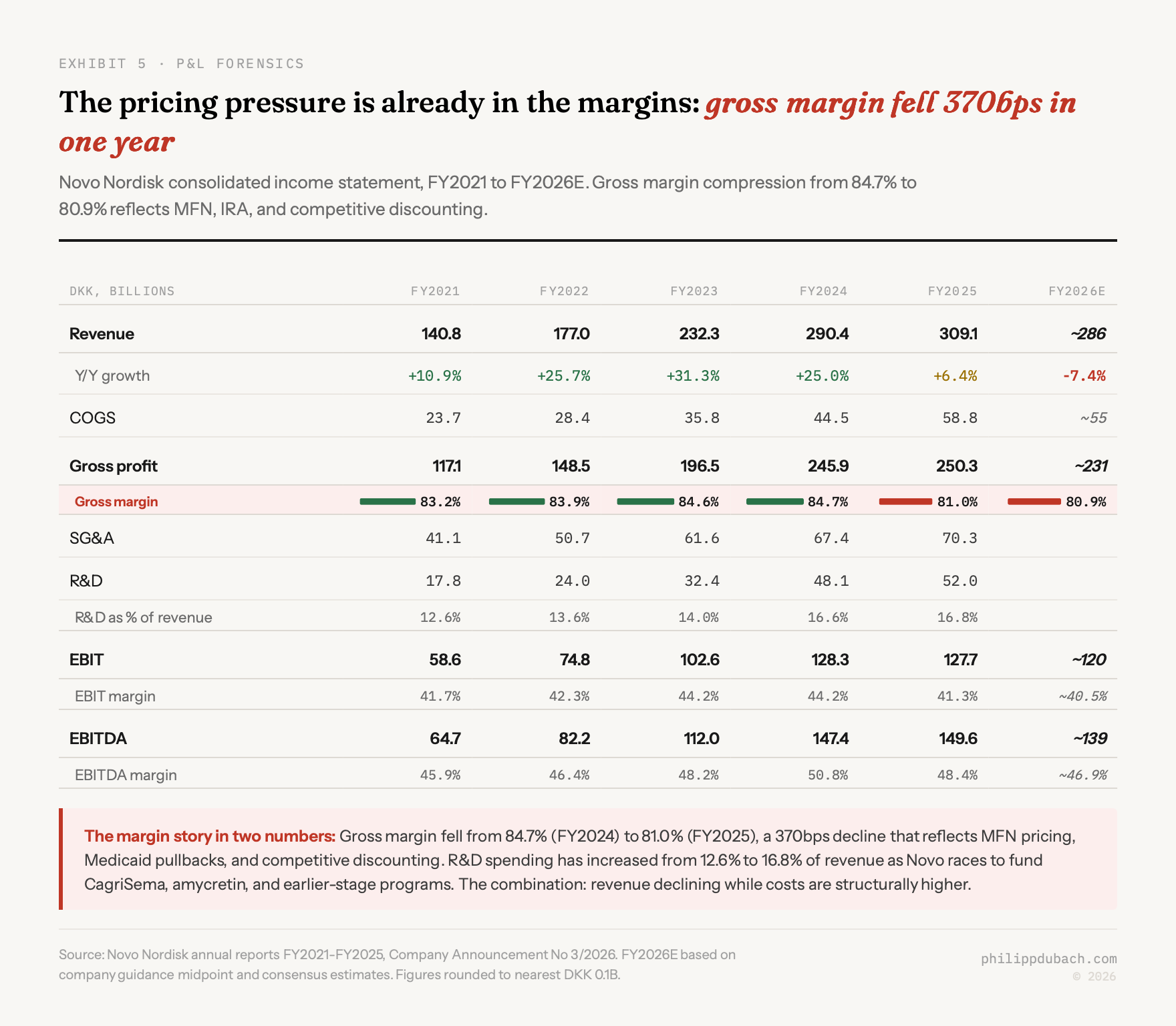

The problems are compounding. US pricing is resetting structurally lower through MFN and IRA. The pipeline just lost its best competitive argument. International patents are falling away faster than expected. Eli Lilly is pulling ahead on every axis. And Novo guided for its first revenue decline in modern history in 2026: adjusted sales down 5-13%. A former senior district sales manager at Novo described that guidance as “very tepid,” and added that the severity of the market reaction suggests investors may be pricing in further downside beyond what management disclosed.

Stock collapse

The speed of the decline matters. In June 2024, NVO hit $142.44. Then, in sequence: a July 2025 guidance cut after Q2 results showed US pricing headwinds worse than expected (shares dropped roughly 22% in a session). A September 2025 announcement of 9,000 job cuts and DKK 8 billion in restructuring charges under new CEO Maziar Mike Doustdar, read not as efficiency but as admission of trouble. February 4, 2026 full-year results guiding adjusted sales growth at -5% to -13% (the stock cratered 18% in Copenhagen). And today, REDEFINE 4.

The 52-week range was $43.08 to $93.80 before today’s open. NVO is now trading around $40, a new low. The all-time high was less than two years ago.

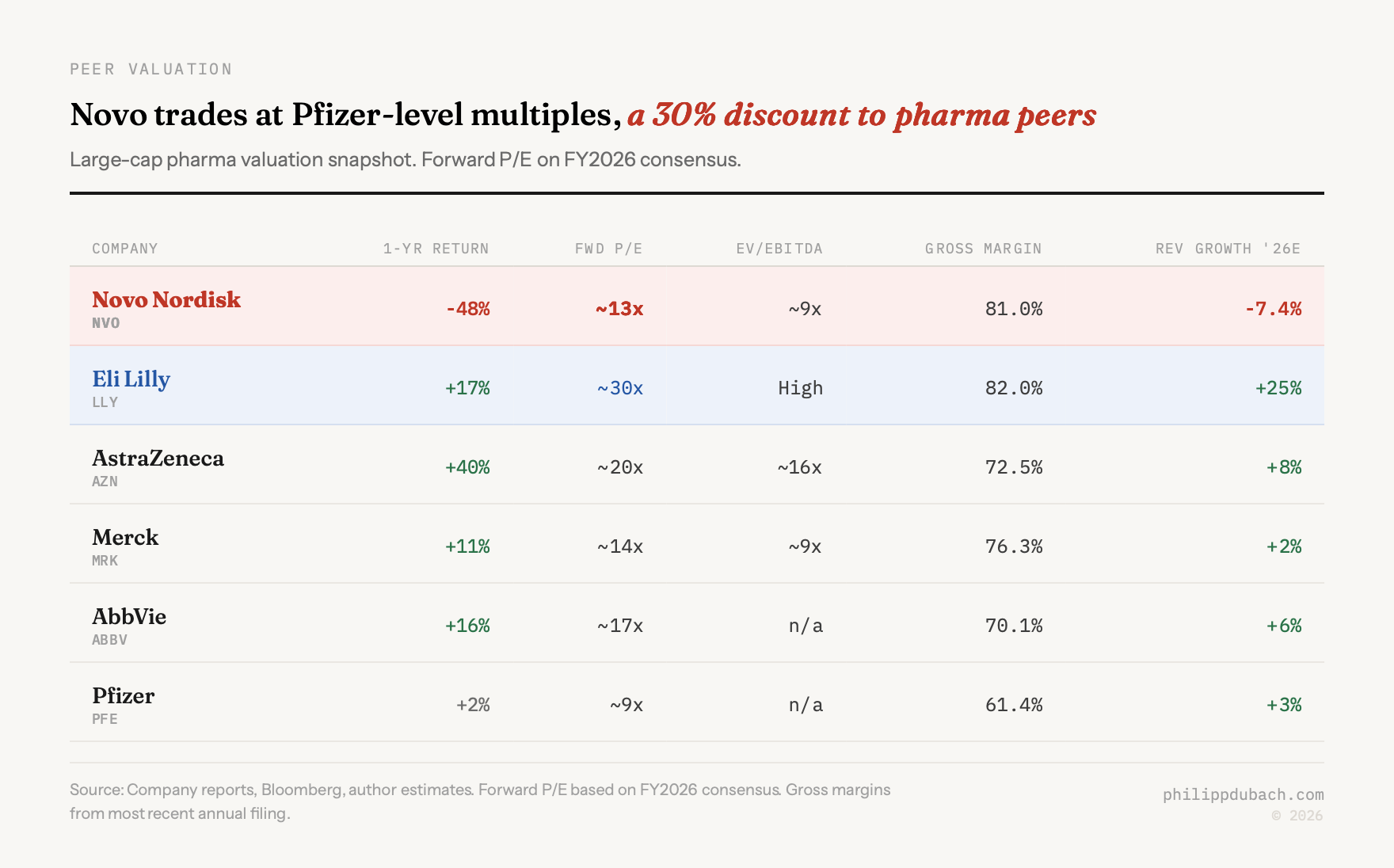

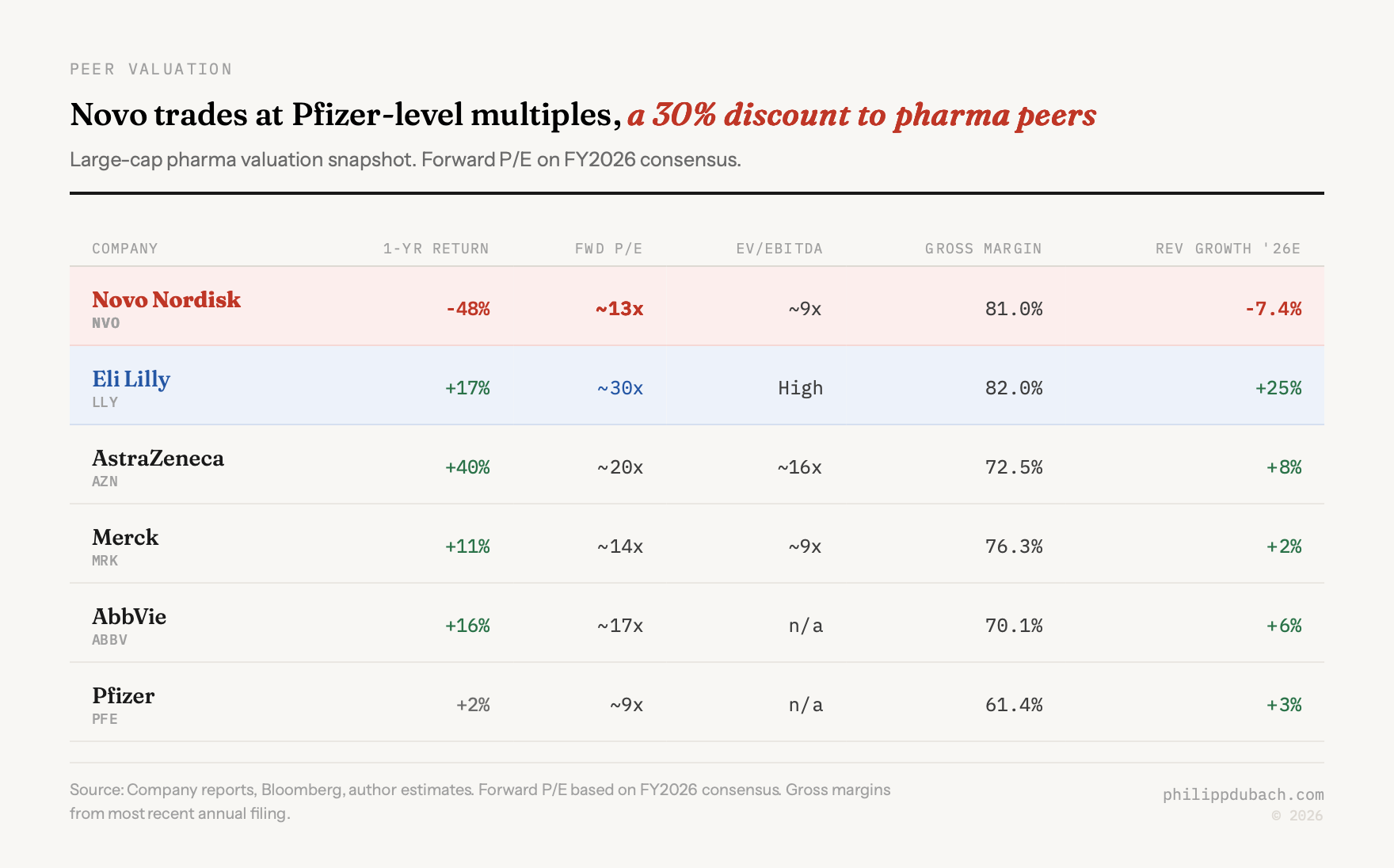

Novo now trades at a lower forward multiple than Merck and below Pfizer, which is dealing with its own post-COVID structural decline. Whether that valuation is justified is the real question.

2026 guidance

It is rare to see a company of Novo’s stature guide for a sales decline. This is not a biotech that lost a coin-flip Phase 3. This is the global leader in GLP-1s telling investors that revenue will shrink.

Three structural forces are driving the decline, each on a different timeline.

The November 2025 MFN deal with the Trump Administration cut Wegovy’s government price to $349/month and set Medicare/Medicaid rates at roughly $245/month, a 60-80% reduction from prior list prices. Insulin was capped at $35/month. Lilly took a similar deal (Zepbound at $346/month), so neither company gained competitive advantage, but both lost pricing power permanently in the government channel. The commercial channel is following. Payers who previously paid $800-1,000 per month for Wegovy are now pointing at the government rate and demanding comparable terms.

Internationally, the patent picture is worse than most investors realize. Semaglutide’s compound patent lapsed in Canada in January 2026 after Novo failed to pay a maintenance fee of roughly CAD 250 (on a self reflective note, maybe this story alone should have made me leave). Sandoz and Apotex are preparing generic launches. Dr. Reddy’s has filed in 87 countries. In China, at least 15 manufacturers are in development. Brazil’s federal court denied a patent extension. The US patent thicket (320 applications, 154 granted, settlements pushing generics to roughly 2031-32) provides breathing room domestically, but international operations generated DKK 112 billion in 2025 revenue, and the erosion has started.

Meanwhile, several states have dropped Medicaid coverage for GLP-1 obesity drugs since late 2025: California, Pennsylvania, New Hampshire, South Carolina. Only 13 states still cover them. The IRA’s Round 2 negotiations, effective January 2027, set Ozempic at $274/month (71% below list) and Wegovy at $385/month. With 2.3 million Medicare semaglutide users, that is a massive revenue compression event arriving in twelve months.

A former director at Novo anticipates strong GLP-1 growth for at least five to seven years but warns that pricing pressures from biosimilars and generics will force significant price cuts in that period. Long-term share, in this person’s view, depends on real-world efficacy and the ability to secure additional indications, not on the brand franchise alone.

CagriSema: a pipeline crisis

I want to push back on the framing already circulating in some analyst notes, which is that REDEFINE 4 is “disappointing but manageable.” It is not manageable. This was the trial that was supposed to prove Novo could compete with Lilly on superior efficacy. It proved the opposite.

The 2.5 percentage point gap on the on-treatment estimand is bad enough. The 3.4 point gap on intention-to-treat is worse, because it suggests CagriSema also has a tolerability or adherence problem relative to tirzepatide. Only 57% of REDEFINE 1 patients reached the highest CagriSema dose, hinting at a ceiling.

A former senior director at Novo expressed disappointment with the REDEFINE trial designs, which allowed for patient down-titration, potentially diluting the efficacy signal. This person regards the asset as safe but questions its commercial strength against aggressive competition. A former Novo advisor was blunter: if Lilly’s retatrutide launches before CagriSema gains traction, it would be a “marketing car crash” for Novo, potentially relegating CagriSema to “second best” status.

Novo’s management pointed to the blinded REDEFINE 11 trial (flexible dosing) and a planned higher-dose CagriSema study as paths to demonstrating “full weight-loss potential.” Maybe. But REDEFINE 11 results won’t arrive until the first half of 2027, and by then Lilly will likely have retatrutide data showing roughly 29% weight loss, plus an approved orforglipron pill without the fasting restrictions.

CagriSema will still probably get FDA approval in late 2026, based on the REDEFINE 1 and 2 placebo data. But launching a drug with clinical proof of inferiority to the market leader is a very different commercial proposition than launching one with a credible superiority story. Pricing, formulary positioning, and physician adoption all get harder. A former director at Eli Lilly told AlphaSense that Lilly’s retatrutide appears superior to both Zepbound and CagriSema based on available data, and that CagriSema lacks a compelling differentiation story, particularly on muscle preservation. The obesity market, this person believes, will double or triple over the next decade, but price reductions will be the primary driver of that expansion.

Eli Lilly is pulling ahead

This is the part I think the Novo bull case underweights. Lilly is pulling ahead on efficacy, pipeline breadth, oral convenience, manufacturing capacity, and patent duration, all at once.

By end of Q3 2025, Lilly held 63% of US branded anti-obesity prescription share and 57% of total US GLP-1 scripts. Zepbound’s Q4 US revenue was $4.2 billion (+122% YoY). Full-year 2025 tirzepatide revenue reached $36.5 billion, making it the world’s best-selling drug molecule. Lilly guided 2026 revenue at $80-83 billion, implying roughly 25% growth. Novo guided for a decline.

Three pipeline assets make the gap worse over time.

Orforglipron, Lilly’s oral non-peptide GLP-1, has an FDA decision expected April-May 2026. No food restrictions, no fasting window. It beat oral semaglutide head-to-head in the ACHIEVE-3 diabetes trial. Goldman Sachs projects 60% oral GLP-1 market share by 2030. An obesity physician familiar with both compounds views the orforglipron launch as a turning point precisely because it lacks the “strict rules” associated with oral Wegovy: fasting, water restrictions, the administration burden that limits real-world compliance. If efficacy is comparable, this person argues, the lower-friction option wins.

Retatrutide, the triple agonist (GLP-1/GIP/glucagon), showed 28.7% weight loss at 68 weeks in TRIUMPH-4. That is 5+ points above CagriSema’s best showing. NDA filing is projected for late 2026. GlobalData forecasts $15.6 billion in 2031 sales.

Manufacturing: Lilly has committed $50 billion+ in investment since 2020, including a $6.5 billion Texas oral pill facility. Tirzepatide patents extend through the back half of the 2030s, giving Lilly 5-7 more years of US exclusivity than semaglutide.

Truist estimates Lilly’s obesity/diabetes trio could reach $101 billion in combined peak sales worldwide, before retatrutide even enters the market.

The Wegovy pill: one bright spot

Credit where it’s due. Oral Wegovy, approved December 22, 2025 and launched January 5, 2026, reached over 170,000 patients within four weeks. Weekly prescriptions hit roughly 50,000 by late January. TD Cowen noted it generated roughly 15x more prescriptions than injectable Wegovy at the same post-launch stage, and double Zepbound’s trajectory.

But about 90% of those prescriptions are self-pay at $149/month, because formulary coverage for the new formulation is limited. That is great for patient access and terrible for revenue per patient compared to the injectable franchise. CEO Doustdar acknowledged the tension: the pill launch is strong, but “the price hit on the existing business trumps the great pill launch.”

Clinically, oral semaglutide 25mg delivers roughly 13.6% weight loss in all-comers, well below injectable Wegovy (roughly 15%) and further below Zepbound (20%+). A former senior diabetes care specialist at Novo expressed skepticism about the oral format’s long-term success, noting the challenging administration requirements contrast poorly with Lilly’s track record of marketing easier-to-take products. A second former specialist at Novo offered the counterpoint: if Novo prices the Wegovy pill aggressively enough, it could capture share despite the convenience gap. The pricing lever is there. Whether management pulls it hard enough, fast enough, is the question.

When orforglipron arrives with comparable efficacy and no fasting requirement, the Wegovy pill’s competitive position narrows. The window is months, not years.

Where I come out

I keep going back and forth on this one, and I think that ambivalence is the right response.

The case for buying: Novo at 11x earnings is pricing in a catastrophe. The GLP-1 market is projected to reach $100-150 billion by 2030. Novo still has the most prescribed semaglutide franchise on the planet. The Wegovy pill launch is legitimately strong. The balance sheet is healthy (debt/equity roughly 0.67x post-Catalent, free cash flow guided at DKK 35-45 billion). The dividend yield is approaching 4%. If the obesity treatment market is multi-winner rather than winner-take-all, Novo at these levels could compound nicely over 5+ years.

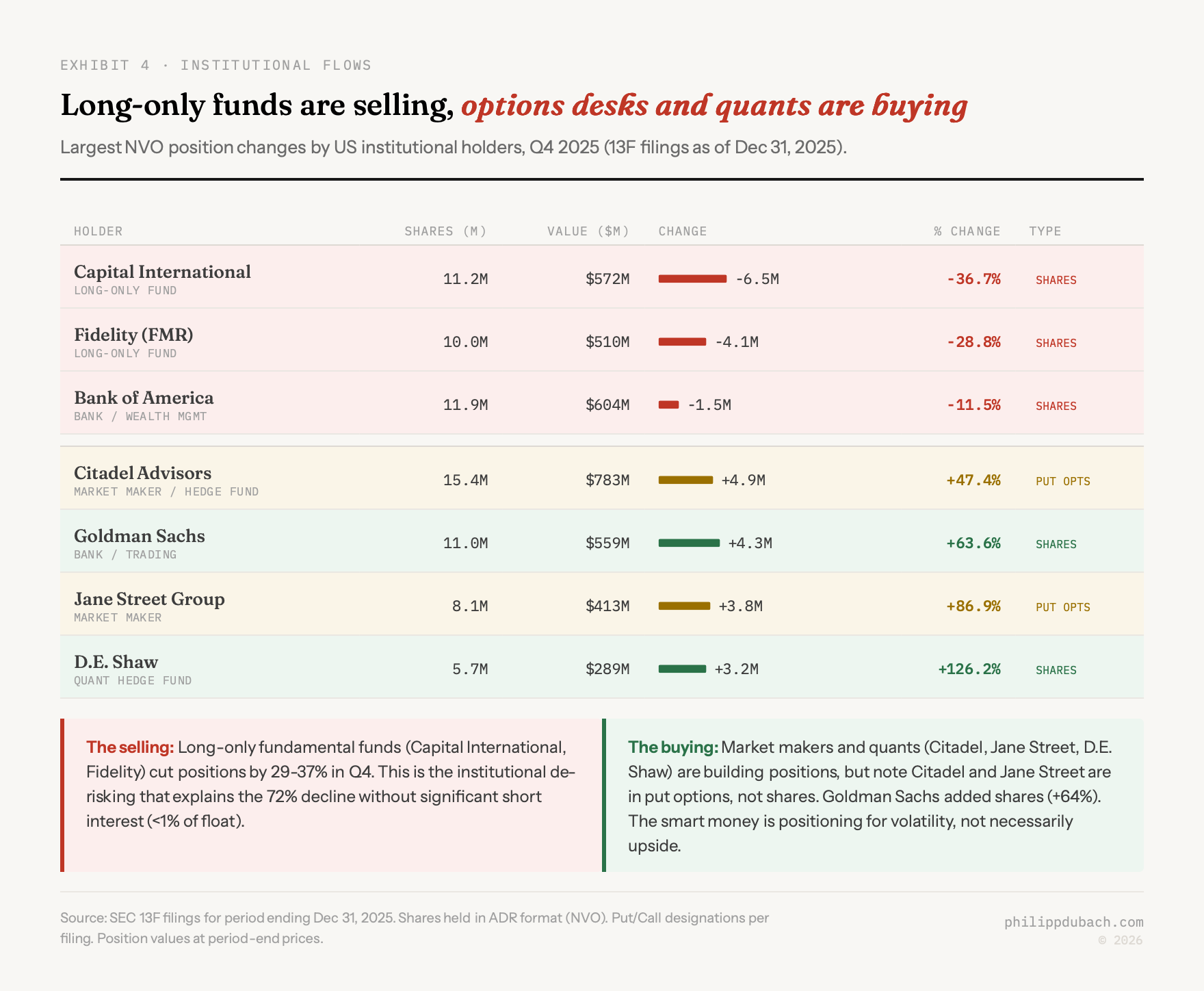

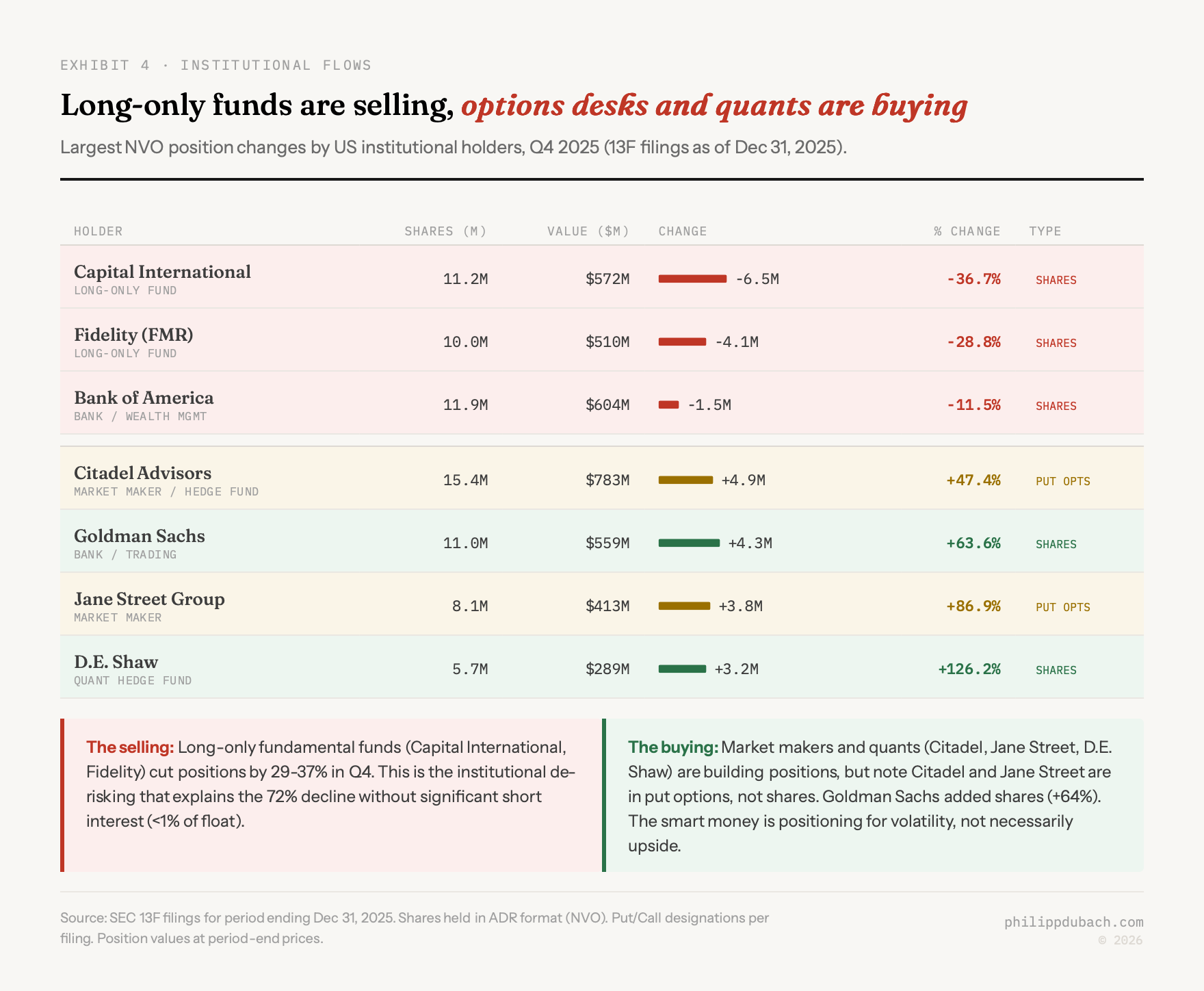

The case for waiting: there is no positive catalyst before May at the earliest. Orforglipron approval could arrive any day and further pressure the oral franchise. Post-CagriSema analyst target revisions haven’t happened yet. European institutional selling may have further to run. Short interest is under 1% of shares outstanding, meaning the 75% decline has been driven overwhelmingly by longs selling, not shorts pressing, with the implication that forced selling from funds that haven’t yet adjusted positions could continue. And the fundamental problem remains: Lilly has proven clinical superiority in injectables, will likely have a better oral, and has a triple agonist coming that makes both companies’ current drugs look modest.

My instinct is that the stock is closer to a bottom than a top, but that the bottom may not be in yet. Forced selling, analyst downgrades from today’s CagriSema miss, and the looming orforglipron approval create a window where further downside is plausible. Barclays noted that some will call the 2026 guide a “kitchen sink” that management will beat, but as they pointed out, the same was said last year and it proved wrong.

For investors with a 3-5 year horizon who can tolerate further near-term downside, this is getting interesting. For anyone who needs to see improving fundamentals before committing capital, there is no rush. The problems I’ve laid out here are structural, and structural takes quarters to fix, not days.