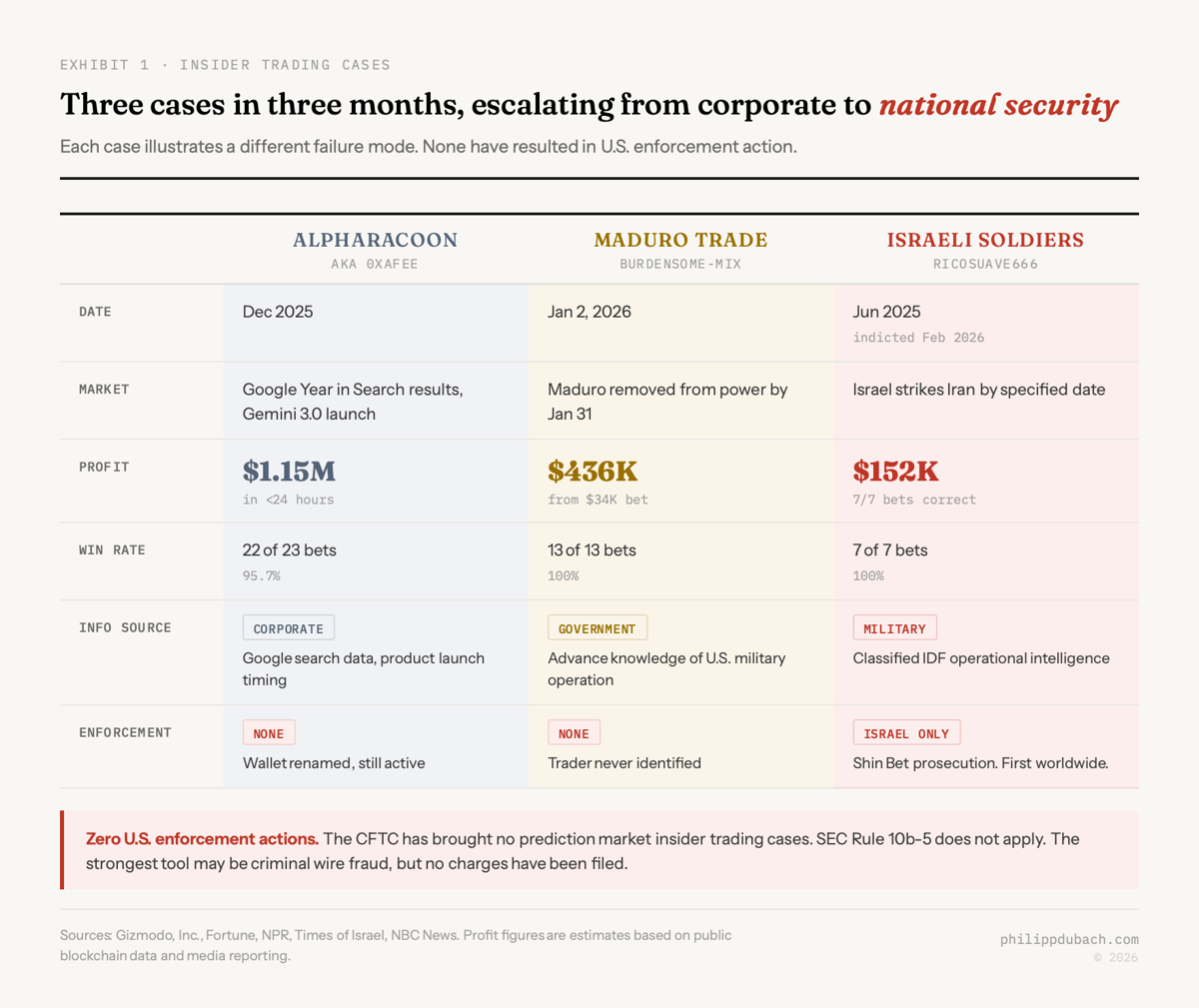

Someone at Google, or close enough to Google, deposited $3 million into Polymarket on December 3, 2025, bet on 23 separate “Google Year in Search” outcomes, got 22 right, and walked away with $1.15 million in profit in under 24 hours. One of those bets: that d4vd would be the most-searched person of 2025, purchased at roughly 5 cents when the market gave it a 0.2% probability.

The wallet, originally called AlphaRacoon, had previously made over $150,000 correctly predicting the exact launch window of Google’s Gemini 3.0 in November 2025. As blockchain engineer Haeju Jeong, who first flagged the account, put it: this is a Google insider milking Polymarket for quick money. The wallet later changed its username to 0xafEe, which might be the most half-hearted attempt at anonymity since an MIT researcher Googled “how sec detect unusual trade” before insider trading.

I’ve been following prediction markets for a while, mostly for the macro forecasting angle, but also because the regulatory ambiguity is fascinating and there are some market inefficiencies worth watching. But the last three months have produced a concentration of insider trading cases that made me want to work through the problem more carefully. The AlphaRacoon case is the most entertaining. The two that followed are more serious.

Three cases, three months, zero enforcement

On February 12, 2026, Israeli authorities indicted two people for using classified military intelligence to bet on Polymarket during Israel’s 12-day war with Iran in June 2025. A Polymarket account called “ricosuave666” placed seven bets on questions like “Will Israel attack Iran on Friday?” and got every one correct. The most profitable single wager: nearly $129,000 that Israel would strike by a specified date. Total winnings: roughly $150,000-$152,000. The Shin Bet, Israel Police, and Defense Ministry called it a real security risk to IDF operations. This is the first criminal prosecution anywhere in the world tied to prediction market insider trading.

In between, there was Venezuela. On the evening of January 2, 2026, an account called “Burdensome-Mix,” created less than a week earlier, placed over $20,000 in bets that Maduro would be removed from power by January 31. Less than an hour after the final bet, Trump ordered the military strike. By 4:21 AM, Maduro was captured. The account’s $33,934 across 13 bets returned $436,759. Chainalysis found the trader cashed out through mainstream U.S. exchanges with no apparent effort to hide their identity. The trader has never been identified.

Each case escalates. AlphaRacoon is someone profiting from corporate knowledge. Burdensome-Mix had advance knowledge of U.S. foreign policy. The Israeli soldiers were monetizing classified operational intelligence during wartime. The surface area for insider trading on prediction markets is, to use the technical term, enormous.

Now there’s an AI that hunts them

Peter Liu, a former Google DeepMind research scientist now co-founding Twenty Labs, published results from Compound AI’s Polymarket integration that systematically detects suspected insiders. The system built a custom database optimized for AI agent queries rather than relying on Polymarket’s rate-limited API. Liu described the agents as “super-human at making data science queries,” noting that each agent operates like 10 concurrent human analysts.

Compound AI independently rediscovered AlphaRacoon despite the username change. More interestingly, it found that AlphaRacoon has friends: a user called “yicici” who made money in the same Google markets, suggesting a coordinated network rather than a lone wolf. When pointed at OpenAI, the system found accounts “oddly good at predicting OpenAI launch dates for models and products,” with at least one that exclusively traded OpenAI events.

It’s not just Compound AI. Polysights, built by 29-year-old Canadian trader Tre Upshaw, has attracted 24,000 users and is closing a $2 million funding round after receiving a $25,000 Polymarket grant. Roughly 85% of flagged trades turned out to be winners. Individual programmers have built copytrading bots that follow suspected insiders, with one reportedly turning $5,700 into $80,000 by tailing signals during the Maduro event.

The irony is rich. Blockchain’s radical transparency, the thing that was supposed to make financial markets honest, is simultaneously enabling insider detection and insider copytrading. The same data pipeline that lets Compound AI catch cheaters also lets copytraders amplify their profits.

Regulation

On regulated stock markets, insider trading law is well-established. SEC Rule 10b-5, decades of case law, a well-staffed enforcement division, cooperation agreements with every broker-dealer in America. Everyone in the industry knows it’s illegal.

On prediction markets, almost none of that infrastructure exists. SEC Rule 10b-5 doesn’t apply because prediction market contracts are swaps, not securities. That puts them under the CFTC, which has historically focused on commodity manipulation (spoofing, cornering), not information-based trading. The CFTC has brought exactly zero enforcement actions for prediction market insider trading.

The CFTC does have Rule 180.1, modeled on 10b-5, which prohibits trading on material nonpublic information. But with a distinction that matters: it requires proof of a breached “pre-existing duty.” In securities law, nearly any MNPI-based trade violates the law. In commodities law, trading on proprietary information is the entire point: a farmer trading grain futures based on their own crop outlook is how the market is supposed to work. Former CFTC Commissioner Caroline Pham has argued that importing securities-law concepts into derivatives markets is analytically confused.

Daniel Barabander of Variant Fund published an analysis on February 6 that crystallized the problem. Insider trading is fundamentally about breaching a promise: a Tesla employee trading on a “Will TSLA beat Q4 estimates?” prediction market violates their confidentiality obligations. But someone who overhears investment bankers discussing a deal at a restaurant generally commits no crime, because no promise exists to breach. Prediction markets, “by making almost anything tradable,” expand valuable inside information into contexts where the existence of any relevant promise is far less clear.

The strongest enforcement tool may be criminal wire fraud. At the Securities Enforcement Forum on February 5, SDNY U.S. Attorney Jay Clayton was asked whether prediction market participants were beyond the reach of fraud statutes. His answer: “No.” Asked whether to expect enforcement actions: “Yes.” But Polymarket’s terms of service don’t specifically mention insider trading, which complicates the wire fraud theory.

Matt Levine, who has written about this topic at least three times between December 2025 and February 2026, puts it best. His core argument: insider trading is not about fairness. It’s about theft. The problem isn’t that you have information the market doesn’t. You’re supposed to try to get information the market doesn’t; that’s the entire point of financial markets. The problem is that you’re using information that belongs to someone else, your employer or client or country, without their permission. You’ve breached a duty.

This framing matters because prediction market enthusiasts instinctively believe insider trading is good for their markets: it makes prices more accurate. Levine acknowledged this directly. But he also identified the fatal flaw: if prediction markets are full of insider traders, there’d be no one to trade against. He estimated that the first 20 people to get arrested for insider trading on Kalshi “will be very surprised.”

Why regulation matters: the lemons problem

The economic case for regulating insider trading on prediction markets goes beyond fairness or legality: it’s about whether these markets can survive.

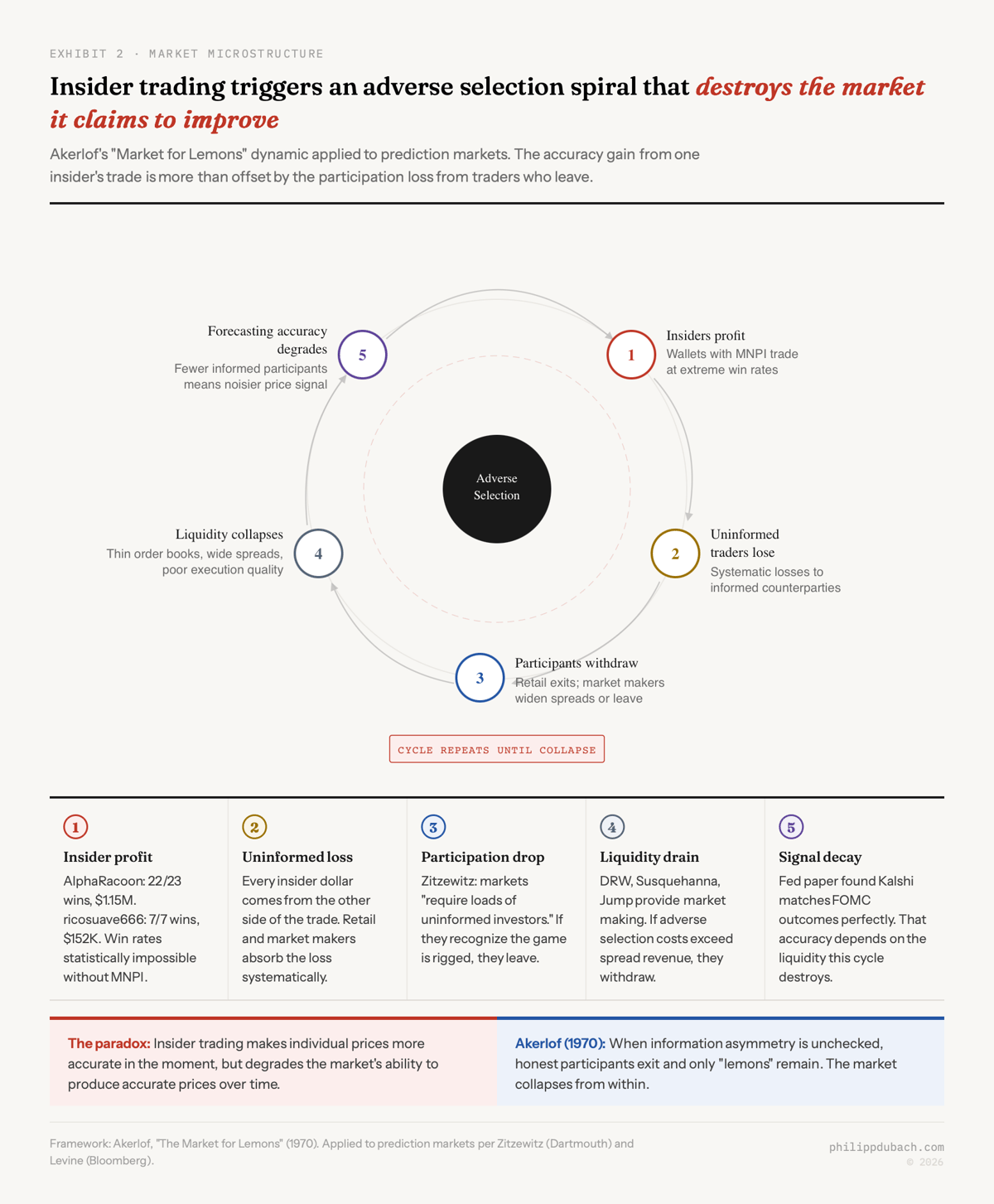

George Akerlof’s 1970 “Market for Lemons” paper described a dynamic where information asymmetry between buyers and sellers causes markets to collapse. When sellers know more than buyers about product quality, buyers reduce their willingness to pay. Honest sellers with good products leave the market because they can’t get fair prices. This raises the average “lemon” rate among remaining sellers, causing more buyers to withdraw. The process continues until only lemons remain.

Applied to prediction markets: if insiders consistently win, uninformed participants recognize they’re trading against counterparties with superior information and leave. Market makers widen spreads or exit entirely. Dartmouth economist Eric Zitzewitz, who studies prediction markets, has stated this directly: prediction markets “require loads of uninformed investors to function” for liquidity. If liquidity providers worry about adverse selection, they provide less liquidity, and any accuracy benefit from insider trading is more than offset by the participation loss.

Wall Street firms are entering prediction markets at speed: DRW is building a dedicated desk at $175,000-$200,000 base salary, Susquehanna became Kalshi’s first official market maker, Jump Trading is taking equity stakes in both platforms, and Goldman Sachs CEO David Solomon has met leadership of both Kalshi and Polymarket. These firms are there to make markets, not to bet on whether Israel will strike Iran. Market makers who systematically take the other side of trades bleed money when their counterparties have inside information. If the institutional players conclude the game is rigged, the resulting liquidity withdrawal would hollow out the market.

Combined Polymarket and Kalshi weekly volume exceeded $6 billion by early 2026. Full-year 2025 volume across all platforms reached approximately $44 billion, a roughly 300x increase from early 2024. Bloomberg terminals now carry prediction market data. CNN struck a deal to integrate Kalshi markets into its coverage.

Prediction markets as macroeconomic forecasting tools

On February 12, 2026, the same day Israeli authorities announced the first-ever prediction market insider trading prosecution, Federal Reserve Board economist Anthony Diercks, along with Jared Dean Katz (Northwestern) and Jonathan Wright (Johns Hopkins/NBER), published “Kalshi and the Rise of Macro Markets” through the Fed’s Finance and Economics Discussion Series. It’s the most thorough empirical study yet on whether prediction markets work as macroeconomic forecasting tools.

The headline finding: Kalshi’s macro markets perform as well as, and in some cases better than, traditional forecasting instruments. For federal funds rate decisions, Kalshi’s median and mode forecasts matched the actual policy outcome on the day before every FOMC meeting since 2022. That’s a perfect record. The mean absolute error for rate forecasts 150 days out was comparable to the New York Fed’s Survey of Market Expectations, a survey of professional forecasters. For headline CPI, Kalshi forecasts statistically outperformed the Bloomberg consensus in certain windows.

The paper identifies a specific structural advantage. Fed funds futures force a binomial assumption: two possible outcomes per meeting. Kalshi’s contract structure assigns nonzero probability to seven or more distinct rate outcomes simultaneously. After speeches by Fed Governors Waller and Bowman, Kalshi markets adjusted the implied probability of a July 2025 rate cut to around 25% within hours. That probability dropped after the June employment report beat forecasts. This is what the authors call “rich intraday dynamics”: the market updates continuously as information arrives, unlike surveys that provide snapshots every six weeks.

The Fed paper is preliminary research, not official policy. But the central bank’s own economists are treating prediction markets as credible information infrastructure. The authors intend to make the underlying data publicly available, which would further normalize prediction market data as a standard input to policy analysis.

If prediction markets are valuable enough that the Federal Reserve is studying them as forecasting tools for monetary policy, the insider trading problem becomes a question of whether a tool the central bank wants to rely on can maintain the informational integrity that makes it useful. Insiders trading on classified military intelligence don’t make the Fed’s rate probability distributions more accurate. They make them less trustworthy.

The regulatory picture, fractured

There are two regulatory tracks, and they aren’t converging.

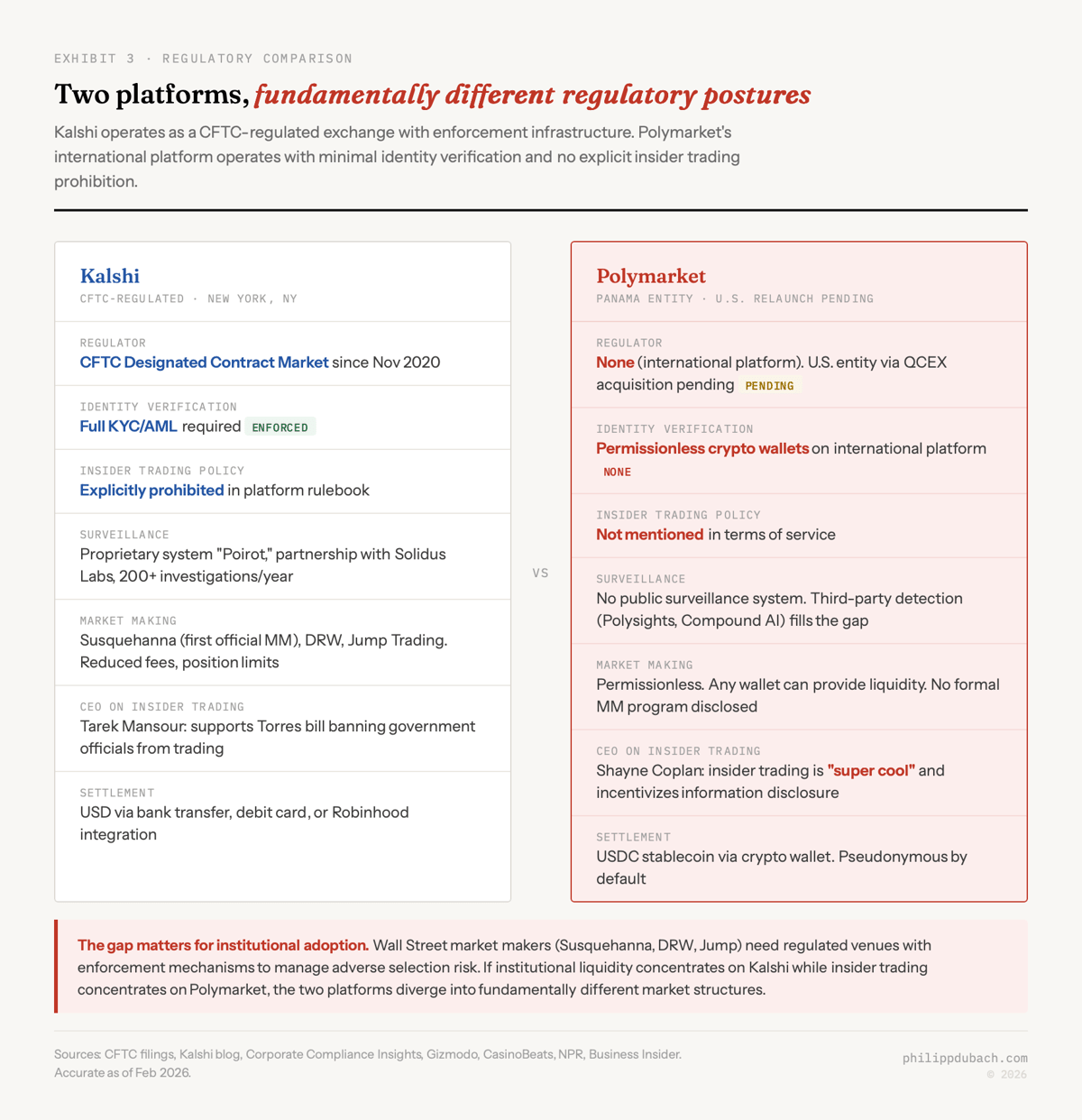

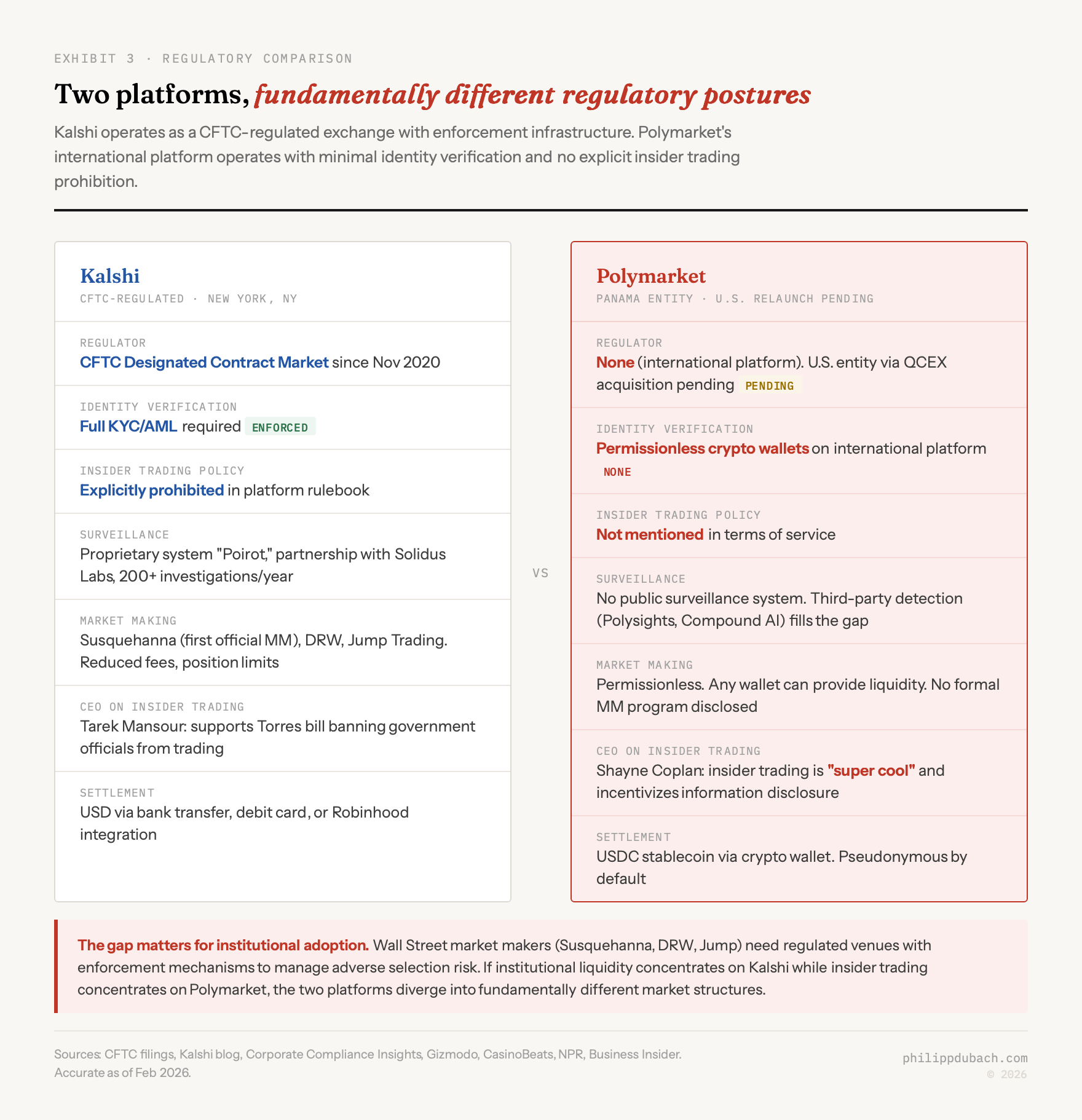

Kalshi is CFTC-regulated, explicitly prohibits insider trading, runs an in-house surveillance system called “Poirot,” has completed over 200 investigations in the past year, and requires KYC/AML verification. Polymarket’s international platform, operated by a Panama-incorporated entity, allows permissionless crypto wallets without identity verification. Its terms of service don’t specifically mention insider trading.

CFTC Chairman Michael Selig, confirmed in December 2025, laid out a four-part plan on January 29: withdraw the Biden-era proposed ban on political event contracts (done February 4), begin drafting new rules, assess ongoing litigation, and support market development. On February 17, he published a Wall Street Journal op-ed asserting exclusive CFTC jurisdiction over prediction markets and filed an amicus brief supporting Crypto.com against Nevada gaming regulators. Selig announced an advisory committee whose planned members include both Polymarket CEO Shayne Coplan and Kalshi CEO Tarek Mansour.

Rep. Ritchie Torres (D-NY) introduced legislation in late January, directly responding to the Maduro trade, that would ban federal officials from trading prediction market contracts related to government activity. The bill targets a real problem, Levine’s point about government officials profiting from events they can influence, but it doesn’t create a general insider trading prohibition. It wouldn’t have stopped AlphaRacoon or the Israeli soldiers.

I’m genuinely unsure where this lands. The libertarian case for prediction market insider trading, that it makes prices more accurate and the market should be a pure information aggregation mechanism, has intellectual appeal. The Akerlof case against it, that unchecked adverse selection destroys the market’s ability to function, has empirical support. The Diercks, Katz, and Wright paper suggests the stakes are higher than either camp acknowledges: these aren’t just gambling venues. They’re becoming part of the plumbing that central banks and institutional investors use to make real decisions.

My instinct, and I want to be honest that it’s more instinct than conclusion at this point, is that the prediction market industry will end up roughly where securities markets were after the Securities Exchange Act of 1934. Some insider trading enforcement is necessary to maintain market integrity, not because trading on private information is inherently wrong, but because without it, the adverse selection spiral will destroy the markets that are otherwise proving genuinely useful. The question is whether that enforcement framework gets built proactively or whether it takes a scandal large enough to force it.

Polymarket’s CEO has called insider trading “super cool.” The Fed is studying his platform’s macro forecasting ability. The Israeli military is prosecuting soldiers who bet on it.