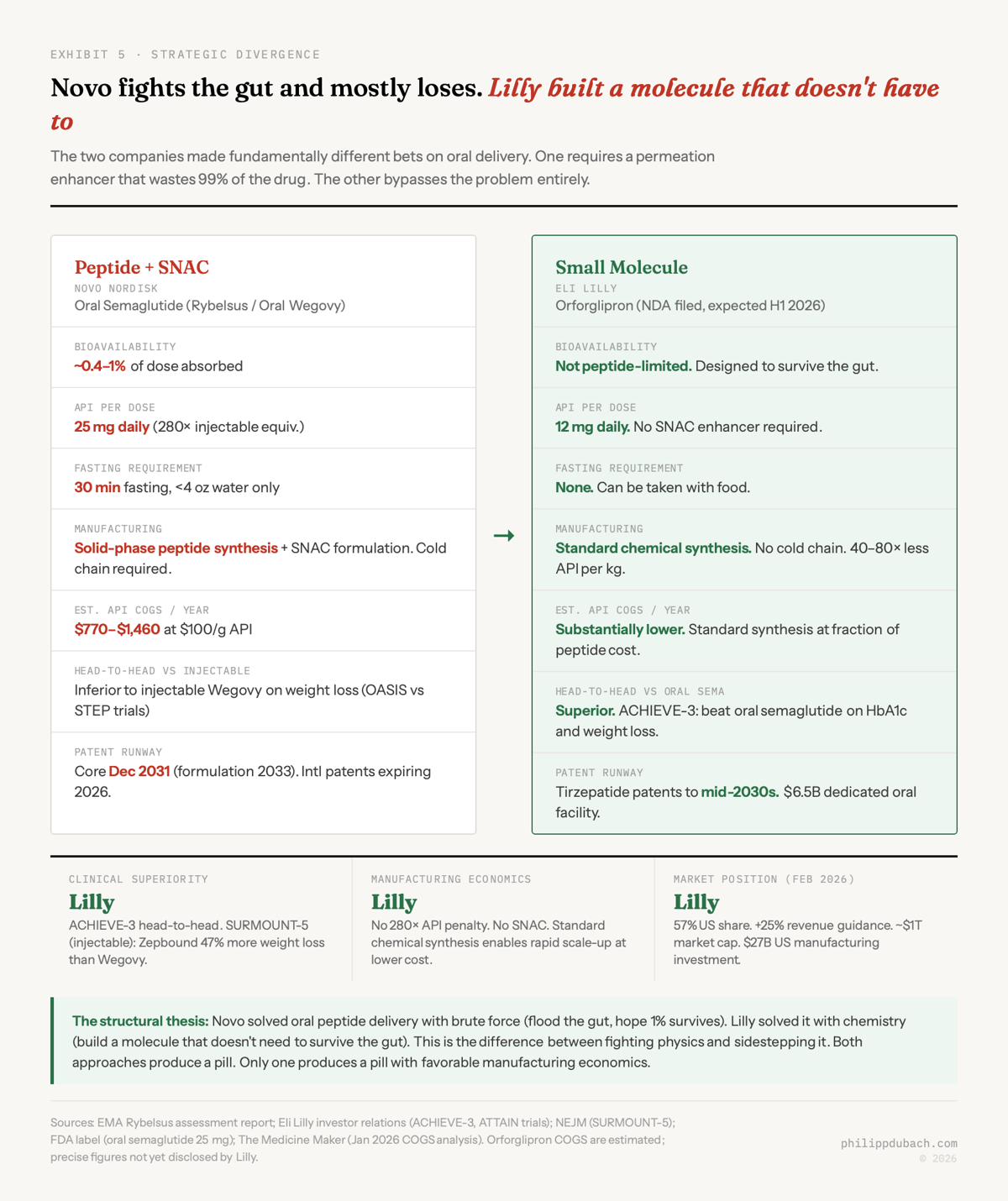

Novo Nordisk spent decades and $1.8 billion learning how to get a peptide past the gut. Eli Lilly looked at the same problem and decided to skip it entirely.

Your gastrointestinal tract is a 30-foot disassembly line for proteins. Acid denatures them, pepsin cleaves them, trypsin finishes the job, and the mucus layer blocks whatever survives. Sean Geiger’s excellent history of oral peptides traces the full arc: the first attempt at oral insulin was in 1922. Over a hundred years and thirteen companies later, no oral insulin exists.

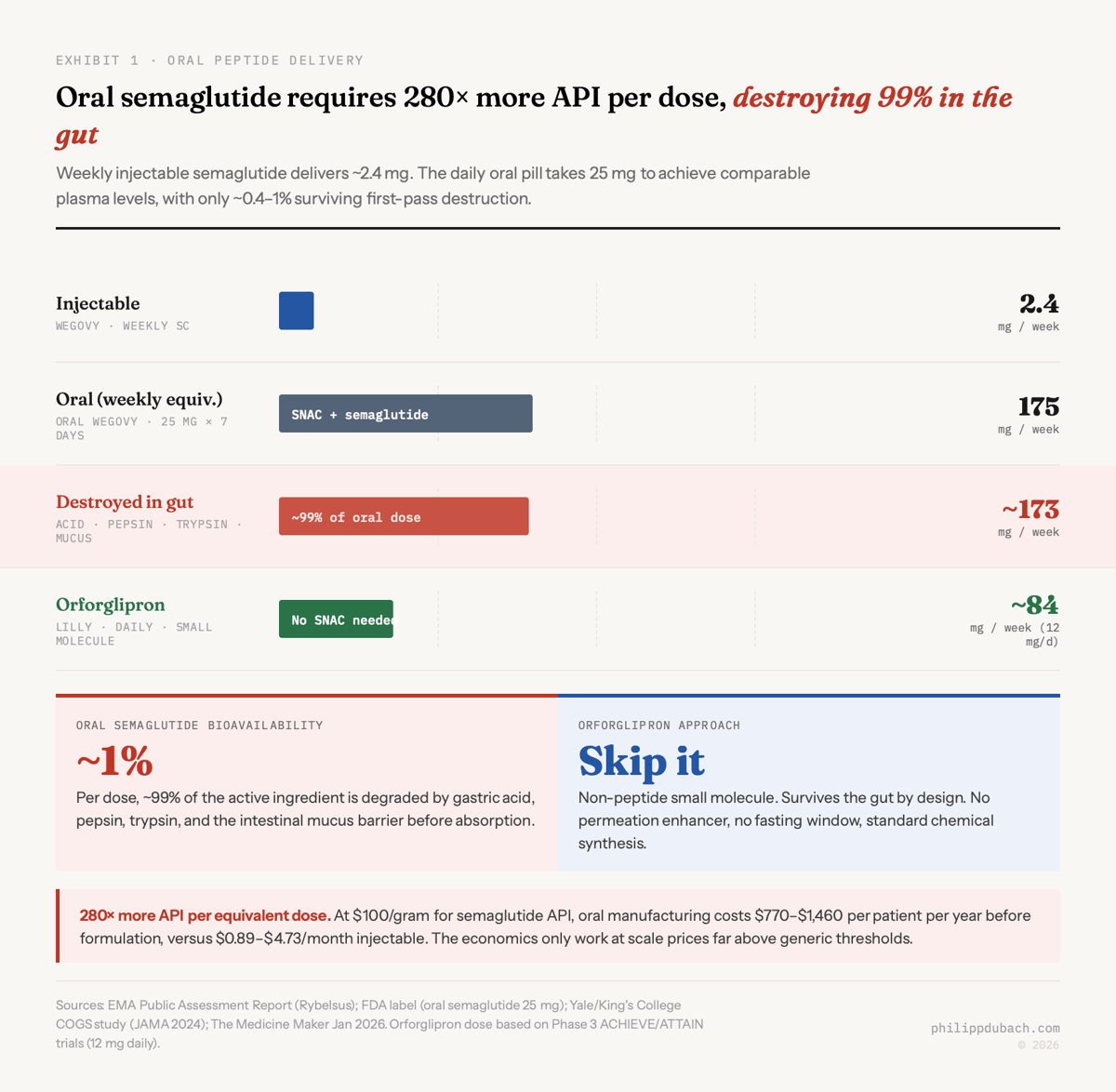

Novo Nordisk spent decades and $1.8 billion acquiring the technology to get around this problem. The result, approved in December 2025 as oral Wegovy for obesity, is a pill that destroys 99% of its own active ingredient before the remaining fraction reaches the bloodstream. The oral 25mg daily dose uses roughly 280x more semaglutide than the equivalent weekly injection. This is the best that peptide oral delivery can do. Eli Lilly decided to skip it entirely, building Foundayo, a small molecule oral obesity drug that isn’t a peptide at all. That divergence in approach will determine who captures the majority of a market that Goldman Sachs projects at $100+ billion by 2030 and that J.P. Morgan estimates will reach 30 million US users within five years.

Oral semaglutide

Sean Geiger’s history of oral peptides traces the science well. The technology that makes oral semaglutide possible is SNAC (salcaprozate sodium), a permeation enhancer developed by Emisphere Technologies starting in the 1990s. Novo partnered with Emisphere in 2007 and acquired the company outright in 2020. SNAC does three things simultaneously: it buffers local stomach pH to suppress pepsin, prevents semaglutide from clumping into inactive oligomers, and temporarily fluidizes gastric cell membranes so the drug can cross. The EMA’s public assessment report puts the resulting bioavailability at roughly 0.4 to 1%. The FDA label confirms: the vast majority of each dose is destroyed.

This creates a problem that’s easy to state and hard to solve. If you need 280x more API per equivalent dose, your manufacturing cost structure looks nothing like the injectable. A Yale/King’s College study published in JAMA found injectable semaglutide costs $0.89 to $4.73 per month to manufacture at the API level. Scale that by 280x and you get oral API costs somewhere in the range of $770 to $1,460 per year, according to The Medicine Maker’s January 2026 analysis. Still below the selling price. But the margin compression is real, and SNAC itself is a costly excipient.

SNAC is also oddly specific. Geiger notes that Novo tried it with liraglutide, a closely related GLP-1 analog, and it failed because liraglutide forms oligomers that SNAC can’t break apart. After over three decades of work, exactly two FDA-approved oral peptide drugs using permeation enhancers exist: Rybelsus/oral Wegovy (SNAC) and Mycapssa (oral octreotide for acromegaly, a different enhancer called TPE). That’s the entire commercial output of the field.

Foundayo: Lilly’s structural advantage

Eli Lilly’s orforglipron, approved by the FDA on April 1, 2026 under the brand name Foundayo, is not an oral peptide. It’s a non-peptide small molecule GLP-1 receptor agonist that activates the same receptor through a different mechanism. Discovered by Chugai Pharmaceutical and licensed by Lilly in 2018, orforglipron requires no SNAC, no fasting window, no cold chain storage, and is manufactured through standard chemical synthesis rather than solid-phase peptide synthesis. The bioavailability problem doesn’t apply because the molecule was designed from the ground up to survive the gut.

The clinical data backs this up. In ACHIEVE-3 (1,698 patients with type 2 diabetes, 52 weeks), orforglipron at 12mg and 36mg was superior to oral semaglutide on both HbA1c reduction and weight loss: the first head-to-head victory over Novo’s oral product. In ATTAIN-2 (obesity with type 2 diabetes), orforglipron delivered 10.5% weight loss at 72 weeks versus 2.2% on placebo. And in ATTAIN-MAINTAIN, patients who switched from injectable Wegovy or Mounjaro to oral orforglipron maintained their weight within 0.9 kg over 52 weeks. A pill that holds the gains of an injection.

Lilly submitted the NDA with a priority review voucher and received FDA approval on April 1, 2026, the fastest approval of a new molecular entity since 2002. Foundayo is available starting at $149 per month for self-pay patients, with savings card prices as low as $25 per month. The company is investing $6.5 billion in a dedicated oral manufacturing facility and $27 billion total in US manufacturing capacity.

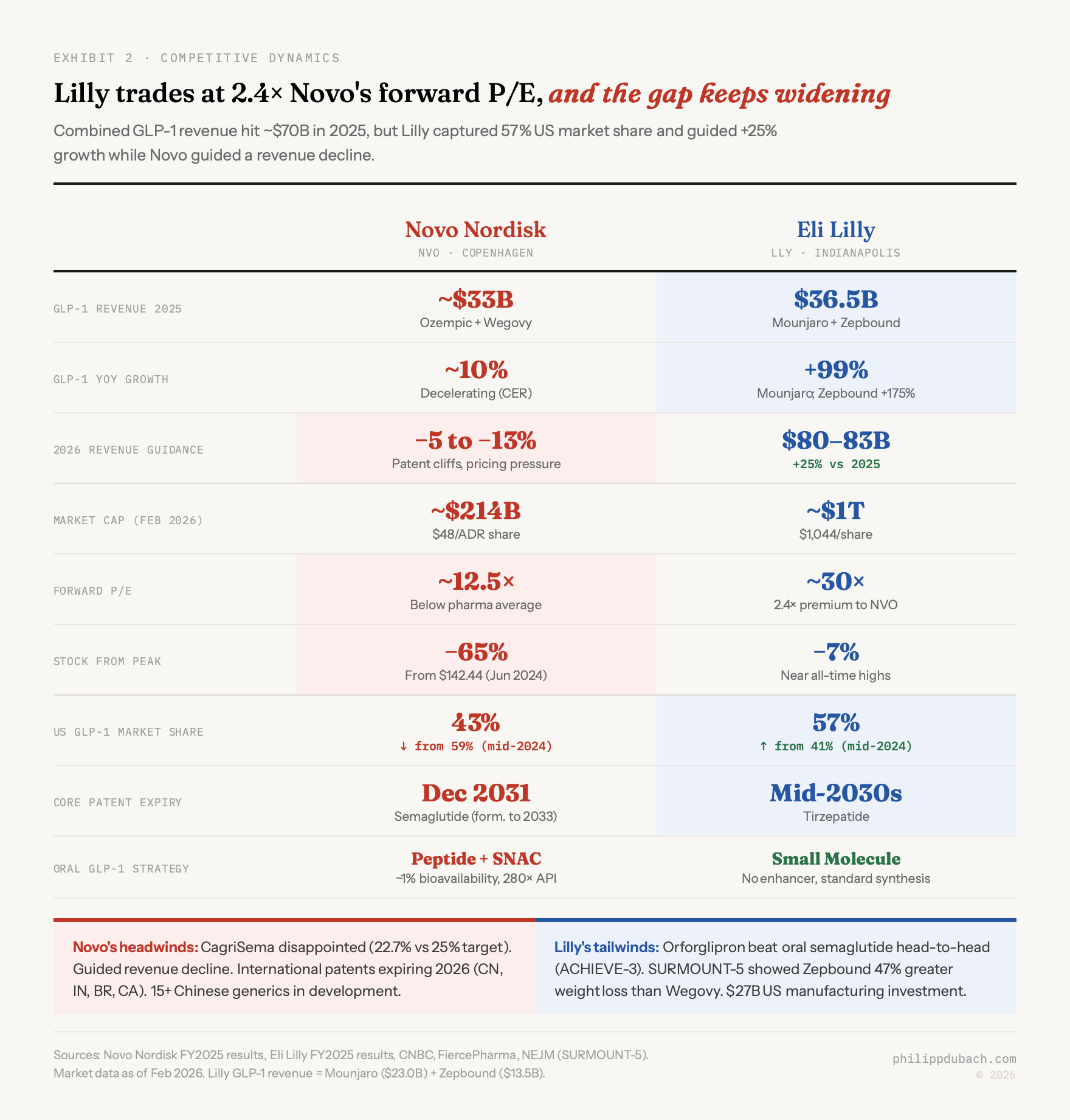

$70 billion duopoly and its widening crack

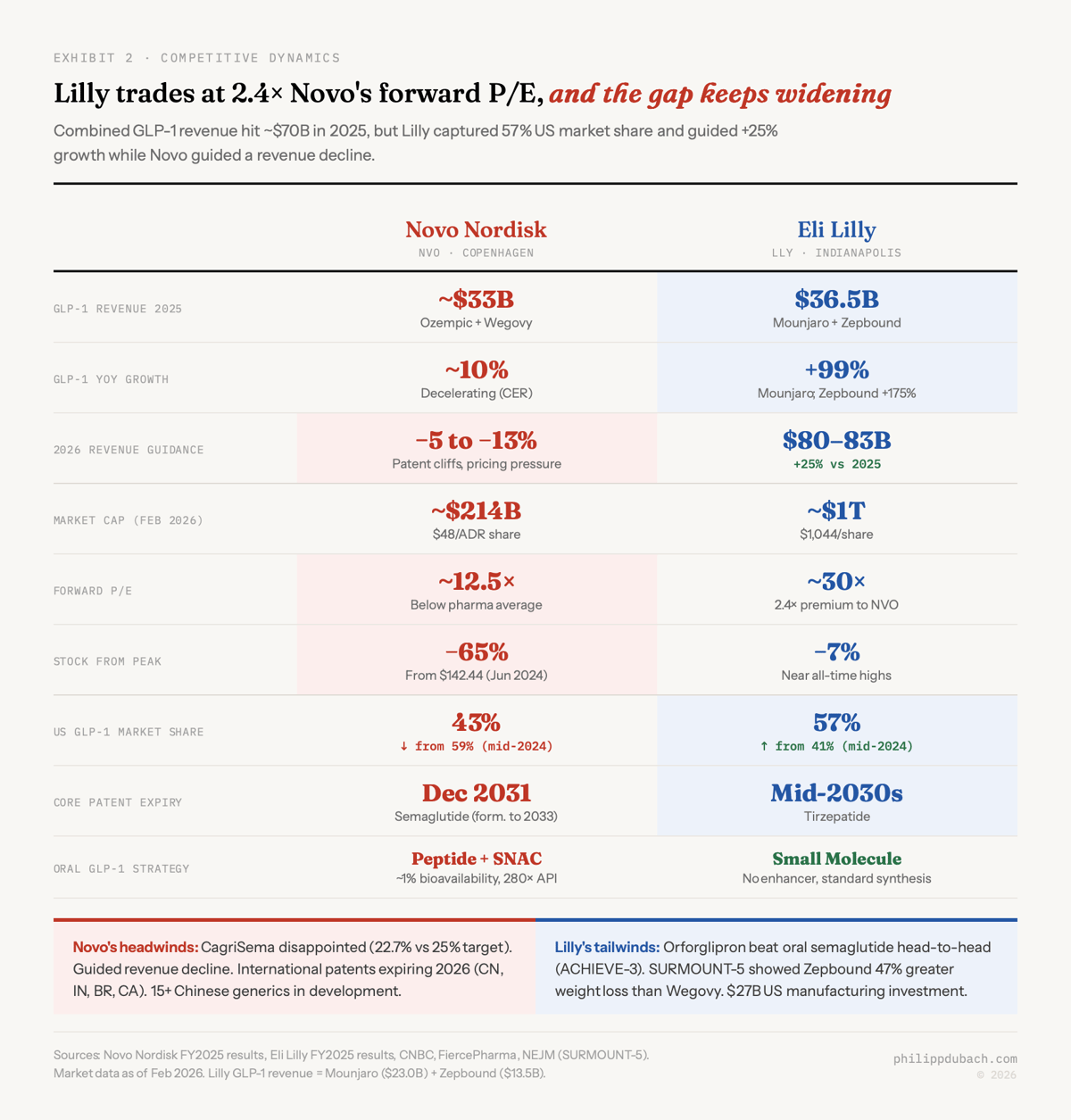

The gap is widening. Combined GLP-1 revenue from Novo and Lilly hit roughly $70 billion in 2025. But the composition shifted. Lilly’s tirzepatide franchise (Mounjaro plus Zepbound) generated $36.5 billion, with Zepbound alone growing 175% year-over-year. Novo’s semaglutide franchise came in around $33 billion, with growth decelerating to roughly 10% in constant exchange rates. Lilly’s US market share hit 57% by mid-2025, up from 41% a year earlier. Novo’s share fell to 43%.

The stock market has been ruthless in pricing this shift. Novo trades at roughly $48 per ADR share, down 65% from its June 2024 peak of $142, a loss exceeding $350 billion in market cap. The company guided for a 5 to 13% revenue decline in 2026, driven by patent expirations in Canada, Brazil, and China, plus pricing pressure from the Trump administration’s drug pricing framework. CagriSema, Novo’s most important pipeline asset, disappointed twice: 22.7% weight loss in REDEFINE 1 (below the company’s own 25% guidance) and 15.7% in REDEFINE 2. Novo’s stock plunged 20% on the first readout alone.

Lilly, by contrast, guided 2026 revenue at $80 to $83 billion, a 25% increase, and trades near $1,044 with a market cap around $1 trillion, the first pharma company to reach that level. Forward P/E: roughly 30x versus Novo’s 12.5x. That 2.4x valuation premium reflects a simple thesis: Lilly has the better drug (Zepbound showed 47% greater weight loss than Wegovy in the SURMOUNT-5 head-to-head), the better oral pipeline, and the longer patent runway (tirzepatide patents extend into the mid-2030s versus semaglutide’s core US patent expiring December 2031, with biosimilar competition likely following shortly after).

The Hims & Hers saga sits at the chaotic edge of all this. HIMS launched a $49 per month compounded oral semaglutide pill on February 5, 2026, using unproven liposomal technology with no published bioavailability data. Within four days, HHS had referred the company to the DOJ, Novo had filed a patent infringement lawsuit, and HIMS had suspended the product. Novo’s CEO alleged independent testing of compounded samples showed impurity levels as high as 86%. What happens when the incentive to undercut $1,000-per-month pricing collides with the actual difficulty of making peptide drugs work orally.

Does Oral Delivery Commoditize GLP-1

Does oral delivery commoditize GLP-1s, or does it expand the market so dramatically that even with pricing pressure, the opportunity grows Early evidence already supports the expansion thesis: Novo’s oral Wegovy pill uptake is running roughly 10x higher than the original injectable Wegovy launch, drawing in new patients rather than converting existing injection users.

The statin precedent is the strongest data point we have. After generic atorvastatin launched in 2011, total statin use expanded from 31 million to 92 million Americans by 2019, a 197% increase. Total prescription volume grew 77%. The per-unit price collapsed, but total market volume more than compensated. Updated clinical guidelines, lower copays, and reduced patient resistance combined to pull in millions of people who would never have started therapy at the original price and delivery format.

Current penetration is absurdly low: fewer than 5% of eligible US adults are on anti-obesity medication therapy, against 104 million with obesity. At statin-like penetration rates of 35% or higher, that’s a 5 to 10x expansion. Persistence data reinforces the point: only 32% of obesity patients persist at one year and 15% at two years. Side effects account for 43.7% of discontinuation, financial barriers for 30.9%. Adherence collapses when the friction is high. An oral weight loss pill that’s cheaper, eliminates the injection barrier, and has no fasting restrictions (orforglipron) attacks all three.

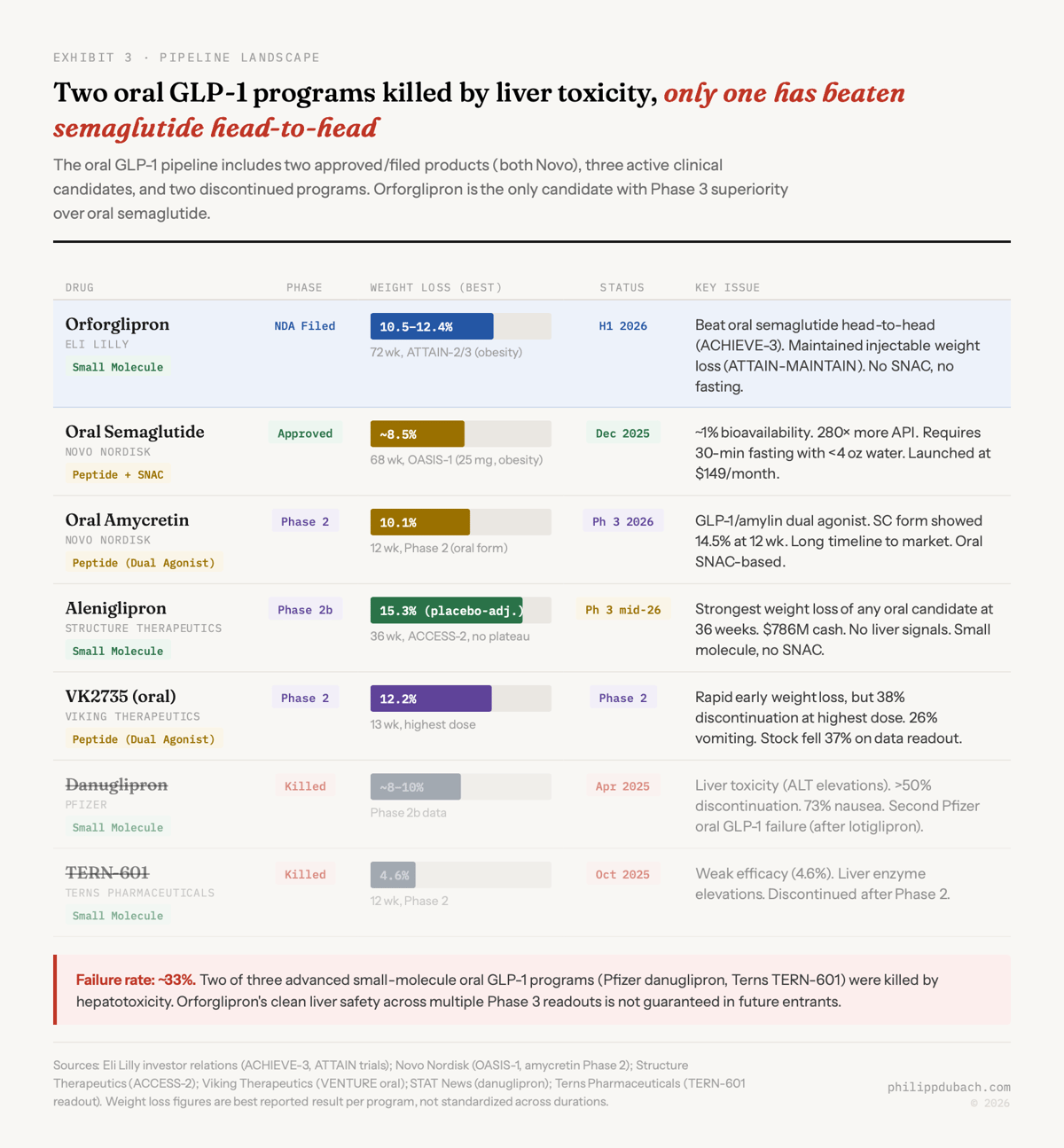

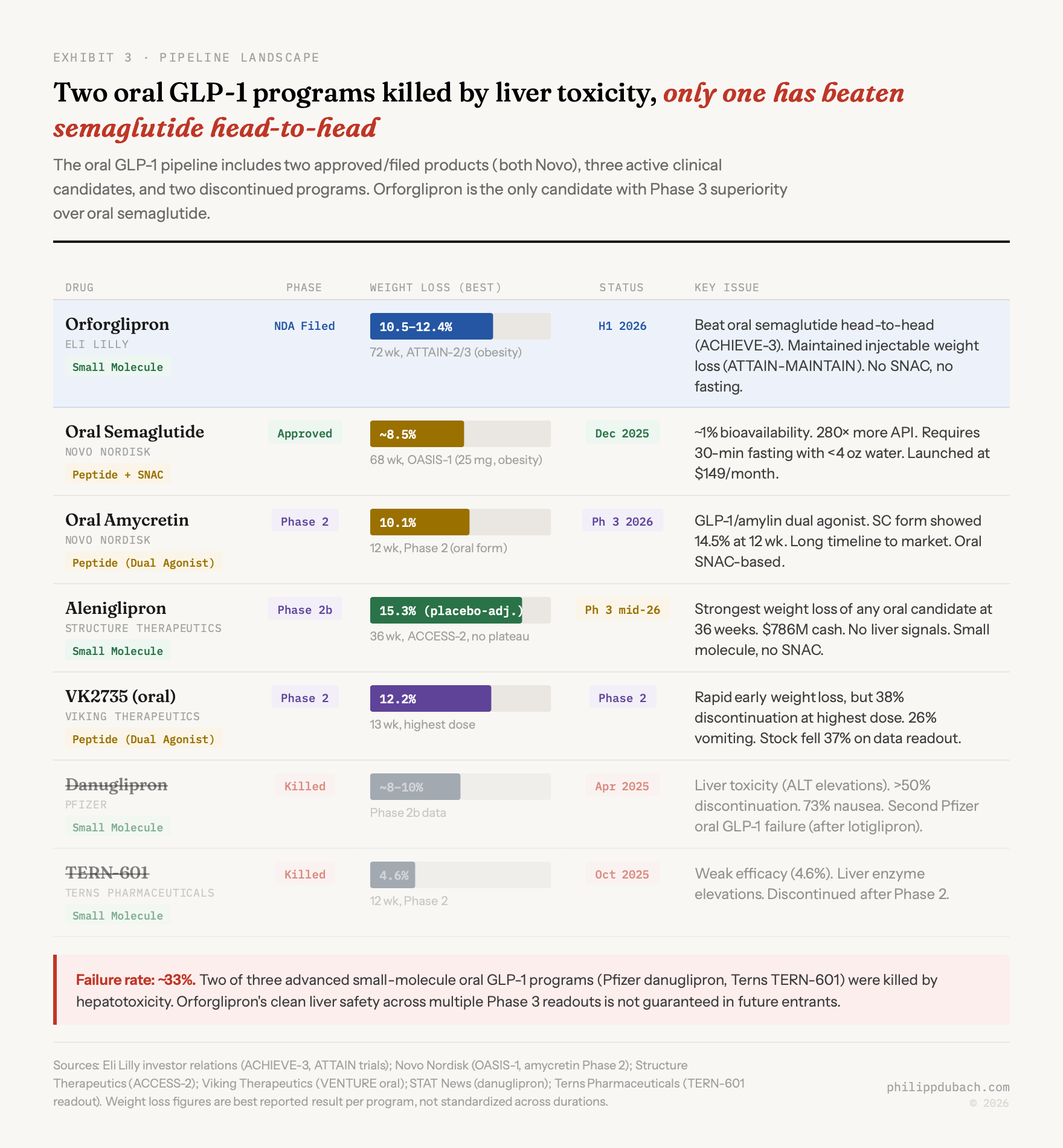

Oral GLP-1 pipeline

The rest of the oral GLP-1 pipeline is worth tracking but the outcomes are uncertain. Viking’s oral VK2735 showed rapid weight loss in Phase 2 (up to 12.2% at 13 weeks) but a 38% discontinuation rate at the highest dose sent the stock down 37%. Structure Therapeutics’ aleniglipron posted 15.3% placebo-adjusted weight loss at 36 weeks in Phase 2b, competitive numbers with no plateau, and has $786 million in cash to fund Phase 3. Pfizer’s danuglipron was killed by liver toxicity in April 2025, the second Pfizer oral GLP-1 failure. Terns Pharmaceuticals also exited after weak Phase 2 data and liver enzyme elevations. Behind them, Novo’s oral amycretin, a GLP-1/amylin dual agonist, enters Phase 3 in 2026 and could offer best-in-class weight loss if the oral formulation holds up. Oral small molecule GLP-1 development has a meaningful failure rate, and Foundayo’s clean safety profile across multiple Phase 3 trials is not something I’d assume the next entrant can replicate.

The thing that makes this market so interesting is that almost every important variable is in motion at the same time: form factor (injection to pill), pricing structure ($1,000 per month to $149 to potentially lower), patent protection (expiring internationally, holding domestically), competitive dynamics (Novo decelerating, Lilly sprinting with Foundayo, Hims imploding), and the macro question of Medicare coverage. I’m more confident in the structural thesis, that oral GLP-1s expand the market through a Jevons-like dynamic, than I am in picking the right entry point for any individual stock. But if forced to bet on which company is best positioned for that expansion, the answer seems clear. Lilly built the molecule that doesn’t need to fight the gut. Novo built one that fights and mostly loses.

At 30x forward earnings for Lilly and 12.5x for Novo, there’s a version of this where Novo is the contrarian value play and Lilly is priced for perfection. I don’t think that’s the right framing. I think Novo is cheap because it has structural problems, the worst kind of cheap, and Lilly is expensive because it has structural advantages, the best kind of expensive.